This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The insurance representative tried to explain that many of the denials were because most policies do not cover flood. Our firm was asked to represent a … The post Florida Policyholders Are Upset with Stupid Denials of Claims appeared first on Property Insurance Coverage Law Blog.

All insurance policies include a section placing specific responsibilities and obligations on policyholders to act in a certain way before entitling them to policy benefits for what should be a covered loss.

First, this case strongly reminds policyholders to be aware of time limits in their insurance policies and take action as soon as they believe their claim is not being handled fairly.

All insurance policies include a section placing specific responsibilities and obligations on policyholders to act in a certain way before entitling them to policy benefits for what should be a covered loss.

First, this case strongly reminds policyholders to be aware of time limits in their insurance policies and take action as soon as they believe their claim is not being handled fairly.

Florida’s largest insurer, has suspended policy binding ahead of predicted Hurricane Helene, and a board member asked if the carrier could do more to help policyholders manage flood insurance claims from the looming storm. Citizens Property Insurance Corp., “My question …

In yesterdays post, Policyholders and Public Adjusters Often Need to Hire Their Own Experts, the court found that the insurance policy did not provide coverage for the claimed damages for two primary reasons.1

Property insurance adjustersboth company-employed and independentserve as the backbone of the claims process, ensuring that policyholders receive the full benefits of their coverage as swiftly and fairly as possible.

Property insurance adjustersboth company-employed and independentserve as the backbone of the claims process, ensuring that policyholders receive the full benefits of their coverage as swiftly and fairly as possible.

A recent ruling by a federal trial court stated that the policyholderclaimed that a severe hailstorm on May 28, 2021, caused extensive damage to his property, including damage to the roof, vents, flashings, windows, window screens, fascia, gutters, downspouts, and HVAC system. appeared first on Property Insurance Coverage Law Blog.

This is Florida law regarding when an insurance company must start investigating an insurance claim: 3)(a) Unless otherwise provided by the policy of insurance or by law, within 7 days after an insurer receives proof-of-loss statements, the insurer shall begin such investigation as is reasonably necessary unless the failure to begin such investigation (..)

A recent Indiana Court of Appeals decision where Merlin Law Group’s Ed Eshoo was counsel for the policyholder provides a textbook example of how an insurance company’s conduct can waive strict policy requirements, even when attempting to preserve those rights through reservation letters.

When policyholders file an insurance claim, they expect their insurer to pay losses. Most policyholders have never read their policy nor would appreciate what it even means with nuanced coverage causation rules applying that vary from state to state.

Consequently, the plaintiff was not entitled to indemnity for damage to the property it purported to insure under a commercial property insurance policy. [1] During the policy term, the business claimed that the properties suffered damage caused by a hurricane and submitted a claim to the insurer. Hawley Insurance Co.

California fire insurance policies must provide an insured a minimum of 12 months from the inception of the loss to bring any suit or action on the policy for recovery of any claim. Code 2071.

In my basic course about property insurance coverage to public adjusters, and as a standard issue regarding case intake at Merlin Law Group, I first emphasize to always make certain the named insureds and clients have a right to bring the claims. appeared first on Property Insurance Coverage Law Blog.

Simply mailing a cancellation notice to a policyholder, when viewed in the context of other indicators, was enough to comply with state law and void a homeowner’s insurance policy shortly just weeks before a fire destroyed a home, the North …

A recent viral social media post following the California wildfires has brought to light a critical issue: homeowners are finding their insurance claims denied because their properties are held in trusts, yet the trusts are not listed on their insurance policies.

They make insureds less likely to file smaller claims because either damage falls within the deductible, or is so close to it that the policyholder would rather not … Deductibles serve several purposes. They provide some premium relief for the insured.

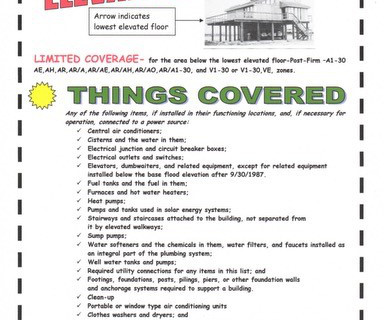

I have received numerous calls from furious Hurricane Helene policyholders after learning how little coverage is afforded for the non-elevated floor of a multi-story building under their flood insurance policies.

Insurance policies that provide broad coverage across multiple items or locations can be a policyholder’s best friend. A recent federal court decision in Louisiana 1 highlights the complexities in determining whether a policy provides blanket or scheduled coverage – a distinction that can significantly impact claim payments.

The Court considered whether the Plaintiffs’ loss was caused by theft or vandalism, as neither term was defined in the policy. In Cheung, the Plaintiffs, who resided in California, purchased property in scenic Mount Vernon, Washington, in July 2021, and insured the property through a policy of insurance issued by Allstate.

While the relationship between tariffs and insurance costs can seem unrelated, tariffs can increase costs for insurers and policyholders. Read more to understand this relationship and how agents can help policyholders manage this uncertainty. This drives up the cost to repair, impacting claims costs.

Insurance affordability in Georgia is dwindling as claim frequency and insurer costs soar, according to the latest issue brief from Insurance Information Institute (Triple-I), Trends and Insights: Georgia Insurance Affordability. Injury claim severity in the state is slightly higher than in the rest of the country.

June 24, 2024) offers valuable lessons for policyholders regarding the importance of cooperation in the insurance claims process. Following the hurricane, plaintiff submitted an insurance claim with a detailed contents list for $663,682 in personal property losses. LEXIS 111077 (W.D.

A recent viral social media post following the California wildfires has brought to light a critical issue: homeowners are finding their insurance claims denied because their properties are held in trusts, yet the trusts are not listed on their insurance policies.

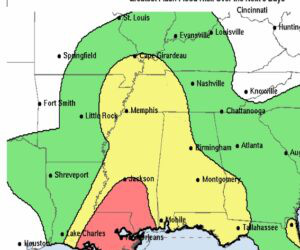

Mississippi’s insurance commissioner is reminding policyholders that once Hurricane Francine moves across Louisiana, it will likely bring strong winds and heavy rains to the western part of the Magnolia State. And residents should be prepared by reading their insurance policies, …

Ending a putative class action, the United States Court of Appeals for the Fifth Circuit examined policy language and two statutes to hold that an insurer does not owe sales tax on top of an actual cash value payment. The policyholder’s contract provided: Limit of liability A. The address shown in this policy. July 24, 2024).

Establishing strong, trusting policyholder relationships drives long-term success for many agents and brokers. However, these relationships can also lead to unintended risks, like the possibility of E&O claims if professional boundaries are missed. This can help reduce misunderstandings that often lead to E&O claims.

With each expansion, we refine our underwriting models in real-time, anchoring our promise to swiftly pay claimsover $250 million disbursed to datewhen policyholders need us most. These deployments supercharge data-driven underwriting, expedite claims management, and deliver real-time insights for brokers and policyholders worldwide.

At issue in the case was the application of the policy’s wear and tear exclusion and its exceptions. The insurance policy covered direct physical loss but contained an exclusion for physical damage caused by wear and tear, marring or deterioration.

If the debris removal program is genuinely available at no cost to all Los Angeles County residents, it should not affect their insurance claims, said Commissioner Lara. The California Department of Insurance worked closely with local, state, and federal leaders to ensure that the programs costs are not deducted from insurance benefits.

Every part of the insurance lifecycle is changing in the digital age, including the handling of claims. Agents and brokers play important roles in the digital claims management process, from educating policyholders on loss mitigation to helping insureds file claims and work with their insurers.

But these policies may not always offer the levels of protection purchasers think they do. Cyber operations can be conducted by state-sponsored groups, independent hackers, or criminal organizations that may claim to act on behalf of a sovereign power and its political objectives.

Both resolved and unresolved violations can affect the terms, premiums, and overall coverage of these policies. Brokers also help interpret legal precedents and case law, including issues of negligence, duty to maintain clauses, and the concealment or misrepresentation clauses found in insurance policies.

Top Coverage, Top Service A Chubb Masterpiece Homeowners Insurance policy provides outstanding protection for your home as well as providing exceptional service. Processing of a claim is efficient and speedy. If you have a loss of any kind, Chubb will send an adjuster to assess damage right away.

By Max Dorfman, Research Writer, Triple-I The total value of lightning-caused homeowners insurance claims rose more than 30 percent in 2023, to $1.27 billion from $950 million in 2022, Triple-I estimates based on national claims data provided by State Farm. The number of claims rose 13.8 of Claims Avg.

Learn more about how to help policyholders prepare for the unexpected with helpful tips. How to Help Policyholders With Proactive Disaster Planning An important start to disaster planning is considering whether or not a potential loss would be covered by insurance. Provide expert educational services for policyholders.

Our Claims Partner, Aspray, Wins Loss Assessor of the Year 2024 We are delighted but not surprised to announce that our claims partner, Aspray, has won the prestigious “Loss Assessor of the Year 2024” award at the British Claims Awards. Key Factors Behind Aspray’s Success 1.

Additionally, even if insurance is provided, policies may come with exclusions that specifically limit coverage for risks related to unresolved violations. Both resolved and unresolved violations can affect the terms, premiums, and overall coverage of these policies.

Shield Insurance Blog | Small Insurance Claims | Contact Our Sales Team! Small Insurance Claims Can Raise Premiums Small insurance claims, such as those for minor property damage, may seem like a hassle to deal with. However, filing small insurance claims can have long-term financial consequences.

Both resolved and unresolved violations can affect the terms, premiums, and overall coverage of these policies. Brokers also help interpret legal precedents and case law, including issues of negligence, duty to maintain clauses, and the concealment or misrepresentation clauses found in insurance policies.

Filing a commercial claim is a complex and daunting process, especially for business owners unfamiliar with the ins and outs of insurance policies. Inadequate Documentation Insufficient evidence to support the claim can result in it being denied or undervalued. It gives the policyholder and company a favorable outcome.

These wildfires have caused historic damage, claimed lives, and threatened communities. As stories of resilience and courage emerge and the fires are contained, agents and brokers provide critical insurance support for policyholders. When consumers do not carry sufficient insurance coverage, everyone is at risk.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content