This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As insurers look to 2025, several trends are emerging that affect premium and deductible costs — leading to lengthy conversations between insurance agents and brokers and their customers. For worship facilities, some of the most prevalent trends include: • Weather-related …

Cohen asked the speakers to discuss whether some industry-geography combinations were more palatable for casualty underwriters. Vitulli said there is “relatively good competition” for large accounts with high deductibles. “The market is actively looking to write those. If you’ve got …

Privilege Underwriters Reciprocal Exchange (2024 WL 322297 (Tex. The insurer paid only a portion of the claim because it maintained that the tornado that struck and damaged the property was a “windstorm” and, therefore, the claim was subject to the policy’s “Windstorm or Hail Deductible.” In Mankoff v. Dallas Jan. Loss of Use.

So we must keep in mind that the dividend interest rate leaves out things like underwriting profits and administrative expenses that also affect the final dividend payable to a policyholder. But this is a long standing practice among life insurers that is unlikely to change in the near future.

Many industries are feeling the uncertainty of tariffs and changing trade policies, which can make underwriting more challenging and pricing less certain. This could cause higher rates in commercial property and homeowners lines. This could create the need for frequent rate changes, adding to consumer uncertainty.

It also shows that being aware of any separate deductibles for wind or hail is an important part of assessing your clients coverage options. Human underwriting : Our underwriters assess your risks through discussion, not just algorithms. What Does Distinguisheds Insurance for Apartment Building Owners Cover?

The Hardening Property Insurance Market Since 2017, the property insurance market has been hardening, resulting in lower available limits, higher deductibles and increased premiums. Uneven investment profits causing insurers to pursue underwriting profit, which translates to stricter underwriting criteria and declined submissions.

So this is your premium adjustments, and these are discretionary adjustments that can be given by your underwriter based on how well they perceive you managing your risk, how well they perceive you managing your risk. and why are we gonna try to get this risk up because you’re saying, hey. Say that again.

What are some of the key factors you consider when determining appropriate coverage limits and deductibles? If we are comfortable with our exposure, we may consider increasing the AOP deductible and the theft deductible , depending on the underwriting analysis. So specific to limits, I just mentioned security.

Key Highlights Comparing Medicare Supplement Plans Insurance, or Medigap, helps cover costs that Original Medicare doesn’t, like copays and deductibles. This includes copayments, coinsurance, and deductibles. Medigap plans help you with costs that Original Medicare does not cover, like copayments, coinsurance, and deductibles.

Generally, these policies have higher deductibles than standard policies – $25k, $50k, or $100k are common deductibles. Underwriting is extensive and involves separate applications/questionnaires and an extensive review of historical claims.

Unlike competitors retreating from the market due to aggregation risks, our Fine Art and Collectibles insurance program brings fresh capacity and a willingness to underwrite policies tailored to Californias unique challenges. Wildfire coverage is included under our Fine Art and Collectibles program based on underwriting.

Changes in Underwriting Processes Interest rates can also shape the underwriting processes used by insurance companies. Underwriting involves evaluating risks and determining suitable premiums for policyholders. Moreover, alongside higher premiums, you may encounter an increase in out-of-pocket costs, such as deductibles.

One of the key reasons is lower deductibles, expert knowledge, and tailored coverage options specifically designed for the unique risks faced by public art installations. Flexible deductibles and payment options : Our team collaborates with you to tailor deductibles and payment plans, accommodating your budget without compromising coverage.

In 2018, the 5 th Circuit Court of Appeals took things a step further in Certain Underwriters at Lloyd’s of London v. Depending on the amount of your deductible, this means recovery could be impossible as a practical matter. Lowen Valley View, L.L.C.

Quotes that are ready quickly are usually based on a small subset of information, then the initial baseline quote is refined during the underwriting process. Deductibles 8. You can expect to see an All Perils deductible and/ or a Windstorm/ Hail deductible here, depending on your policy. Insurance Company 2.

Unlike competitors retreating from the market due to aggregation risks, our Fine Art and Collectibles insurance program brings fresh capacity and a willingness to underwrite policies tailored to Californias unique challenges. Wildfire coverage is included under our Fine Art and Collectibles program based on underwriting.

Here are just some of the key benefits you get by partnering with Distinguished: Experienced underwriters : Our underwriters are highly experienced and have the authority to make fast, intelligent decisions, ensuring that your clients receive the coverage they need when they need it.

Here are just some of the key benefits you get by partnering with Distinguished: Experienced underwriters : Our underwriters are highly experienced and have the authority to make fast, intelligent decisions, ensuring that your clients receive the coverage they need when they need it.

With limited access to insurance, affordable housing communities have no ability to negotiate insurance premiums and are forced to pay significantly higher premiums with high deductibles. Some affordable housing community owners and operators reported premium increases of 25-75% due to the presence of pull cords.

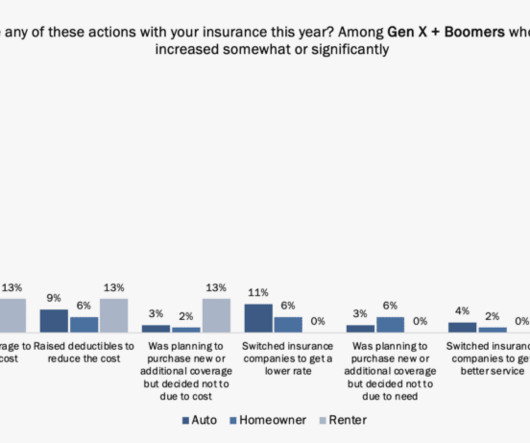

For those who did remain, the most active cost-reducing actions included reduced coverage (auto, 12%; renters, 13%) and raising deductibles (auto, 9%; renters, 13%) which increased their protection gap and could result in challenges for insurers in the future with claims that could ultimately impact loyalty and trust.

Increase Your Deductible: Opt for a higher deductible to lower your monthly premium. Beyond Credit: Other Ways to Save on Home Insurance Improving your credit score is one strategy, but it’s not the only one. Upgrade Your Home: Adding safety features like a security system or fire-resistant materials can reduce risk—and your rate.

automated deductible and Rx updates (so you know when they apply before benefits kick in). W&Bs Underwriting team works directly with carriers to streamline approvals. Well answer all of your and your clients questions about quoting, products, underwriting, sales, enrollment, provider networks, service, claims, billing, and more.

For instance, frequent third-party claims for premises liability may have led to restrictions on Med Pay coverage or a higher deductible to give the customer a bigger stake in safety measures.

Flexible Deductibles and Payment Options : Our underwriting team can take into account your client’s collection, budget, and risk tolerance and design each policy to fit their needs. Our team combines deep expertise across collection categories with flexibility in underwriting and customizing coverage.

That includes understanding what plans offer the lowest and highest out-of-pocket costs, including deductible, copays, and coinsurance. You need to know who offers the products and services that will address your clients’ pain points, objectives, and budget. Ask your Word &Brown rep for details.

The South Carolina Wind and Hail Underwriting Association, also known as Wind Pool, is an association of insurance providers. The South Carolina Wind and Hail Underwriting Association has an eligibility checker. These can include your home’s coverage, deductible, and type of construction.

Additionally, investors can explore the option of higher deductibles to reduce premiums. However, it is crucial to strike the right balance between cost savings and ensuring that the deductible remains affordable in the event of a claim. By assuming a higher portion of the risk, investors may be able to negotiate lower insurance costs.

They explain the details of different policies, including coverage options, premiums, deductibles, and out-of-pocket expenses. Brokers assist clients in deciphering premiums, deductibles, and out-of-pocket expenses, ensuring they understand the full scope of their coverage.

If we don’t get down to addressing the loss ratio — underwriting, pricing, risk selection, and claims management — for many carriers, even if they cut costs by 100%, they’re still not going to be profitable. Their standard coverage would go to customers that wish to cover their deductible.

Anything from quoting to underwriting, servicing, billing or claims may no longer operate at the level expected by customers, putting trust and loyalty at risk. In addition, other actions taken included raising deductibles, particularly for homeowners, and reducing coverage for both auto and homeowners.

The surety’s role is complex, as it must diligently assess the risks associated with underwriting bonds. The insured is not obligated to repay the insurer for the claim payment, except in cases of deductibles, which are predefined portions of the loss the insured agrees to bear.

The Small Business Tax Equity Act would provide an exception into the Internal Revenue Code to let cannabis operators – as long as they’re in compliance with state laws – make the same deductions as any other business. Easier to operate Passage of these laws would make it easier for cannabis-related businesses to operate.

In our 2024 Consumer Research , the top-of-mind issue of finances was reflected in concerns about the increasing cost of insurance and how they were trying to decrease the overall cost with changes in deductibles, lowering coverages and more.

Here are some of the factors our expert underwriters would consider when creating a policy for your client: Collection value: The higher the collection’s appraised value, the more it will cost to insure. Deductible selected: Opting for a higher deductible can lower premiums but increase out-of-pocket costs in case of a claim.

Here are just some of the key benefits you get by partnering with Distinguished: Experienced underwriters : Our underwriters are highly experienced and have the authority to make fast, intelligent decisions, ensuring that your clients receive the coverage they need when they need it.

Small businesses and their employees are no longer subject to medical underwriting for health insurance. The ACA requires marketplace plans to cover at least one drug in each drug class and to include out-of-pocket Rx expenses in an insured persons or familys deductible. Employers with 50+ full-time workers must offer health insurance.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content