This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

By understanding the role fear plays in workerscompensation claims, employers can implement strategies to foster trust, improve outcomes, and reduce costs. The Link Between Fear and Litigation Studies have consistently identified fear as a major driver of workerscompensation litigation. All state laws vary.

Many companies operate under an unwritten rule: accept every workerscompensation claim, no questions asked. A well-managed workerscompensation program should pay 100% of legitimate claimsand 0% of the claims that arent. Claims Reporting Policy : Require employees to report injuries within a specific timeframe (e.g.,

Lets explore the roles of these critical players in a workers’ compensation system. Insurance Company: The Risk Bearer Often referred to as the underwriter, insurer, or carrier, the insurance company provides the workers’ compensationpolicy and assumes the employers risk.

Consider the case of Jane, a worker who sustained a severe back injury. She was given a list of four medical providers but found that: Two providers did not accept workerscompensation patients. One provider accepted workerscompensation but was not taking new patients. Are currently accepting new patients.

These employees, known as “general exclusions,” require their payroll to be reported and calculated separately, directly influencing workerscompensation premiums. ” Stay tuned to complete your understanding and gain further control over your workers’ compensation premiums. All state laws vary.

FREE DOWNLOAD: “13 Research Studies to Prove Value of Return-to-Work Program & Gain Stakeholder Buy-In” Business and Financial Benefits of Transitional Duty Lower WorkersCompensation Costs : Employees who stay engaged at work tend to have shorter claims duration and fewer legal disputes. All state laws vary.

There are elements in your workerscompensation program that may be creating challenges without you even realizing it. These challenges can stem from incentives, employee motivations, policies, or procedures that deliver unintended consequences. View workerscompensation as an adversarial process.

The Solution: Pay Without Prejudice The solution to this prevalent problem is the implementation of a Pay Without Prejudice policy. This policy authorizes payment for medical treatment up to a certain dollar amount (commonly $10,000) regardless of whether the claim will ultimately be denied. All state laws vary.

Revamping a workerscompensation (WC) program can transform how companies manage costs and care for injured employees. Below, we explore common errors and provide actionable steps to begin reforming a workers’ comp program. You should consult with your insurancebroker, attorney, or qualified professional.

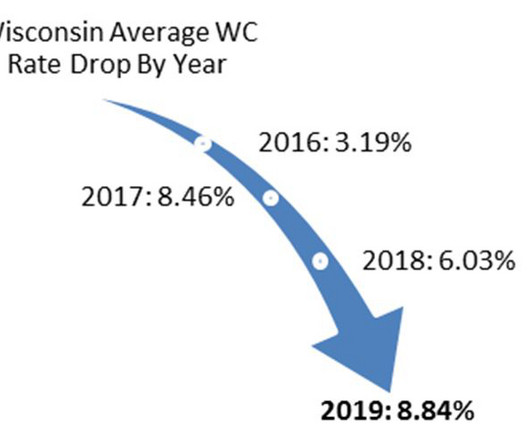

On October 1, 2024 Wisconsin continued its trend entering a ninth consecutive year of reduced workerscompensationinsurance rates. This rate reduction will affect work comp policies with renewal dates between 10/01/24 to 09/30/25. Rates in 2024 fell an average of 10.5% What can Contractors do?

Managing workerscompensation can feel like playing whack-a-mole. One day its a delayed report, the next its an escalating claim or a frustrated injured worker. Transitional Duty Policy Define how employees will return to work, even if modified duty is needed. All rights reserved under International Copyright Law.

By shifting your perspective from compliance-as-burden to compliance-as-advantage, you can leverage OSHA requirements to create a safer, more productive workplace, reduce workerscompensation costs , and enhance your company’s reputation. A policy or training is implemented to check the compliance box. All state laws vary.

” Common Flaws in Policies Many companies unknowingly implement policies that inadvertently sabotage their return-to-work efforts. These flawed policies often prevent employees from returning promptly, which can lead to increased costs and decreased morale. Do not use this information without independent verification.

In the complex world of workerscompensation, risk managers play a vital role in aligning strategic oversight with day-to-day claims operations. Heres a closer look at best practices every risk manager should be following to create a high-performing, cost-effective workerscompensation program. All state laws vary.

Transitional duty keeps injured workers productive and engaged, while helping employers manage workerscompensation costs and maintain continuity in staffing. If no suitable roles are available on-site, remote work such as database clean-up, online training, or policy review might be viable. All state laws vary.

Assignment of Classification Codes Initially, insurancebrokers typically assign classification codes when securing coverage for employers. Brokers discuss the nature of the employer’s work to determine the most suitable code. Upon mutual agreement, the policy is then issued with the corrected classification codes.

This can be done by partnering with clinics or healthcare providers that can see injured workers right away. Clearly define these roles in your RTW policy. Supervisors and case managers should stay in contact with the injured worker to provide support and address any issues as they arise.

How to Protect Your Business Get Comprehensive Insurance Ensure you have general liability insurance, professional indemnity insurance, and workerscompensation if applicable. Consult Legal Experts A business attorney can help review policies, contracts, and risk management strategies to ensure legal protection.

These challenges can be exacerbated by poor communication, lack of clear policies, or inadequate support systems. Develop a Comprehensive RTW Policy A well-defined RTW policy is the cornerstone of managing difficult return-to-work scenarios. You should consult with your insurancebroker, attorney, or qualified professional.

Building on Success: Enhancing Existing Practices Once a comprehensive injury management program is in place, it’s important to build on existing internal processes to closely manage workers’ compensation and improve overall safety outcomes. You should consult with your insurancebroker, attorney, or qualified professional.

Premium Only Plans (POPs): Also known as a Section 125 Cafeteria Plan, a Premium Only Plan enables enrolled employees to pay their health insurance premiums with pre-tax dollars. Plus, your clients can save on Federal Insurance Contribution Act (FICA) taxes and WorkersCompensation.

Click Link to Access Free PDF Download “13 Research Studies to Prove Value of Return-to-Work Program & Gain Stakeholder Buy-In” The Role of Collective Bargaining Agreements Collective bargaining agreements (CBAs) often define the rules and expectations around many employment issues, including return-to-work policies.

If such a captive insures only the risks of its parent or subsidiaries, it is called a “pure” captive. The global insurancebroker and risk advisor’s survey of more than 1,300 captives also shows that gross written premiums in this area grew from $54 billion in 2019 to nearly $61 billion in 2020.

Talk with your clients about their needs, expectations, and budget, as plans that define the insureds inability to perform in their own occupation may be more costly than plans that define disability related to ones ability to perform any occupation. Policies with shorter maximum benefit periods typically have lower premiums.

Rassp, Presiding Judge, WCAB Los Angeles, California Division of Workers’ Compensation Disclaimer: The material and any opinions contained in this article are solely those of the authors and are not the opinions of the Department of Industrial Relations, Division of Workers’ Compensation, or the WCAB, or any other entity or individual.

By Julius Young, Richard Jacobsmeyer, Barry Bloom, Editors-in-Chief for Herlick, California Workers’ Compensation Handbook [Note: This article is excerpted from the upcoming 2025 edition of Herlick, California Workers’ Compensation Handbook. The AI revolution is starting to come to workers’ compensation.

Employers striving to improve their workerscompensation programs often find their goals harder to achieve than expected. The root of the issue is not always poor implementation of return-to-work programs but rather hidden policies or procedures sabotaging progress.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content