This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Many companies operate under an unwritten rule: accept every workerscompensation claim, no questions asked. A well-managed workerscompensation program should pay 100% of legitimate claimsand 0% of the claims that arent. Employees come to believe that every claim will be accepted, regardless of the circumstances.

Third-Party Administrator (TPA): Claims Specialists For employers who are self-insured or insurance companies without an in-house claims department, TPAs play a crucial role. TPAs operate independently of the insurancecarrier, focusing on streamlined claims handling rather than insurance services.

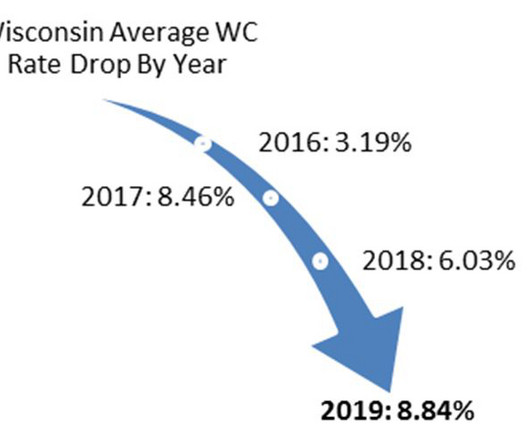

On October 1, 2024 Wisconsin continued its trend entering a ninth consecutive year of reduced workerscompensationinsurance rates. Workerscompensation rates are state mandated in Wisconsin, meaning all insurancecarriers must use the same rates resulting in premiums from one carrier to another are basically the same.

Georgia employers and their workers’ compensationinsurers can rest a little easier after an appeals court this week narrowed the circumstances in which a state guaranty association can seek reimbursement on claims paid after staffing firms’ insurancecarriers become insolvent.

If insurancecarriers want to have dibs on a company’s assets as premium security or collateral, they had better specify that those assets include potential tort-claim settlements, a federal appeals court said Wednesday. In a case that involved a Florida …

As a result, the workers’ compensationinsurancecarrier decides not to pay for the treatment until they determine the claim’s compensability. Simultaneously, because the injury was reported as work-related, John’s group health insurance also refuses to cover the treatment.

Defending workers’ compensation claims from employees who have not disclosed previous injuries may have just become a little more complicated for employers and insurancecarriers in Georgia. The Georgia Court of Appeals last week found that a long-standing defense against …

Joseph notified either NJ Transit or its carrier of the third-party action, nor does the opinion discuss what, if anything, the third party attorney knew about NJ Transit’s lien when the third party case settled. in workers’ compensation medical and temporary disability benefits to petitioner, Darshelle Joseph.

These matters must be considered when seeking to maximize the efficiency of any workers’ compensation program and reduce costs. Consider Vocational Retraining Retraining is a dirty word in workers’ compensation, given the expenses associated with the process. Evaluate the various options.

Work-related disability is covered by WorkersCompensationinsurance. A person cannot generally qualify for both WorkersCompensation and STD for the same incident. The California SDI program is administered by the states Employment Development Department (EDD).

Insurancecarriers often offer access to risk management tools, training programs, and support lines to help companies prevent and effectively manage employment-related issues. Having an EPLI policy helps alleviate these financial burdens and allows businesses to focus on their operations rather than on legal troubles.

Although your policies may limit or exclude certain coverages, some insurancecarriers have policies with sublimits and carvebacks for certain expenses that may provide some relief. Consider the following questions as you build your plan: How are executives and managers communicating the strategy to workers on the front lines?

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content