This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Americas housing market is teetering on the edge of a crisisa situation fueled by climate change, soaring insurance premiums, underinsurance, and systemic failures in addressing these growing risks.

While the relationship between tariffs and insurance costs can seem unrelated, tariffs can increase costs for insurers and policyholders. Read more to understand this relationship and how agents can help policyholders manage this uncertainty. Here are some ways agents can help: Educate policyholders about costs and rising premiums.

This brief provides an overview of how several factors, including skyrocketing costs from litigation, pose risks to coverage affordability, availability, and other potential economic outcomes for Georgia residents. Data indicates that litigation costs have become a pervasive concern for risk management.

To shed light on these challenges and offer guidance on navigating this complex landscape, Risk Strategies Mike Vitulli, Zurich North Americas Bill Chepulis, and Zywaves Jim Blinn and Jeff Cohen recently participated in a webinar titled “Casualty Craziness: Whats the Cause and Whats the Cure.”

Rather, new technology presents opportunities to facilitate more proactive and individualized risk management than ever before, while also enabling employees to do what this industry does best: engaging with other people.

The Birthday Rule is gaining traction across the country, allowing Medicare Supplement policyholders to switch plans without medical underwriting around their birthday each year. Reduced underwriting can lead to higher premiums , increased policy lapses, and fewer carriers remaining in the market. in 2024 vs. 13.0% in 2024 vs. 13.0%

Social inflation and E&O risks are connected as agents must manage policyholder expectations even as claims costs rise, premiums remain high, and denials are issued for claims policyholders expected to be covered. Learn more about social inflation and E&O risks and how to manage these concerns.

But with growth opportunities comes risk. We’re prepared to help you grow your distribution network, power your decision making with industry-leading data and insights and empower your teams and policyholders with industry knowledge and expertise. And your own first-party data isn’t going to get you there.

Claims-related litigation has significantly declined over the past two years, and premium averages are nearly flat, with several insurers requesting rate decreases from the states insurance regulator. This competition from the private market has allowed policyholders to leave Citizens Property Insurance Corp.

Additionally, defects in windows, doors, handrails, and stairs not only contribute to drafts and security concerns but also increase the risk of falls. Blocked emergency exits or fire escapes and electrical hazards, including exposed wiring or overloaded circuits, further compound these risks.

While the perception of overall severe weather risks varies significantly by region, 65 percent of the participants nationwide believed their home is at risk from thunderstorms, according to the new report, Catastrophic Weather Events and Mitigation: Survey of Homeowners by the Insurance Research Council (IRC), a division of The Institutes.

But it’s important to remember that the crisis wasn’t created overnight and that it will take time for the reforms and other developments to be reflected in policyholderpremiums. One factor keeping upward pressure on rates is fraud and legal system abuse. With only 15 percent of U.S.

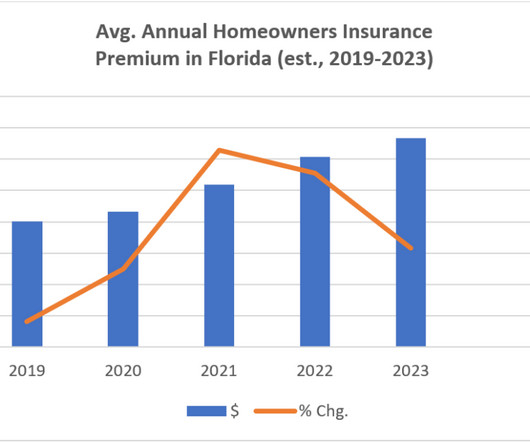

Homeowners insurance premium growth in Florida has slowed since the state implemented legal system abuse reforms in 2022, according to a Triple-I analysis. As shown in the chart below, average annual premiums climbed sharply after 2020. In 2022, average homeowners premium rates rose more than 17 percent, to $3,040.

However, for agents and brokers, these new AI-driven processes can introduce new E&O risks to mitigate and manage. Learn more about managing new E&O risks introduced by AI to ensure AI remains an asset, not a liability. Some of the new risks include: AI-generated quotes may be mispriced or contain incorrect details.

Independent P&C agents and brokers who reside and work in this region must also know how to help policyholders manage earthquake risk. This requires experience, expertise, and a proactive approach to risk management and mitigation. Learn more about how agents can help their policyholders manage earthquake risk in this blog.

Driven by rapid advancements in technology, shifting risks, and increasing policyholder expectations, the industry will likely have different products and services by the time 2025 draws to a close. Read more about 2025 insurance trends and consider how these risks and opportunities may impact your agency.

Insurers view these violations as signs of deferred maintenance and increased risk. Even if some violations are eventually addressed, a history of non-compliance can still lead to higher premiums. Both resolved and unresolved violations can affect the terms, premiums, and overall coverage of these policies.

In a recent interview with Triple-I CEO Sean Kevelighan, Harger discussed the importance of preparing for and preventing damage from this risk, which is second only to flooding when it comes to costly weather events. When installed properly, lightning protection systems are scientifically proven to mitigate the risks of a lightning strike.”

Mold & Water Damage are also major concerns; leaks or excessive moisture can lead to mold growth that poses health risks. Additionally, Electrical Hazards like exposed wiring or unpermitted electrical workpose serious safety risks. Insurers view these violations as signs of deferred maintenance and increased risk.

In Chicago, housing code violations not only affect tenant safety and property values but also play a critical role in insurance risk assessments. Then there are electrical hazards , such as exposed wiring or faulty outlets, which pose serious safety risks. Structural problems are also a significant concern.

The Insurance Act 2015 IMPORTANT INFORMATION – PLEASE READ Duty of Fair Presentation The Insurance Act 2015 imposes an obligation on all policyholders to “make a fair presentation of the risk” prior to the policy commencing. What happens if I do not fairly present the risk? What is a reasonable search?

The homeowners insurance market is complicated and dynamic, and many policyholders have experienced increased rates in recent years despite no changes to their coverage or claims filed. Even among typical homeowners policies, premiums likely increased year over year. Reduce liability risks. billion each.

With infractions ranging from heating failures to illegal conversions, understanding these issues is essential for assessing risk and underwriting policies. This can pose serious health risks for tenants and lead to significant liabilities. Insurers view these violations as signs of deferred maintenance and increased risk.

Inflation drives up property valuations , construction costs , and insurance premiums. This has resulted in higher premiums and limited coverage in catastrophe-exposed areas. Insurers are investing in advanced technology and data analytics to improve risk assessment and underwriting processes.

.” Rather than forcing a rigid, one-size-fits-all approach, these companies are tapping into new technologies to craft customized insurance packages for each consumer’s unique needs and risk profile. And get this some even let you pay as you go instead of heavy annual premiums. However, it has significant limitations.

How Interest Rates Influence Insurance Costs Insurance premiums are sometimes indirectly influenced by interest rates. Here’s how: insurers rely on investment income to keep premiums competitive. When interest rates rise, the returns on these investments can increase, potentially affecting premium rates.

Small Insurance Claims Can Raise Premiums Small insurance claims, such as those for minor property damage, may seem like a hassle to deal with. Many policyholders may be tempted to file a claim for every little incident in the belief that their insurance policy will cover all damages.

By understanding key terms, policy details, and the rights and responsibilities of policyholders, consumers can engage with insurers more effectively, ensuring better communication and ultimately achieving their desired outcomes. By exploring these guides, individuals can gain a comprehensive understanding of why insurance is essential.

By Lewis Nibbelin, Guest Blogger for Triple-I Home and auto insurance premium rates have been a topic of considerable public discussion as rising replacement costs and other factors – from climate-related losses to fraud and legal system abuse – have driven rates up and, in some states, crimped availability and affordability of coverage.

The concept of speed is increasingly becoming an important competitive factor when presenting rating information for specialty insurance risk coverage. Insurance risks are diverse and ever-evolving, especially specialty insurance, which plays a crucial role in providing coverage for unique and high-risk situations.

” or can’t get the insurance you deserve for that matter – insurance with reasonable premiums and without unnecessary restrictions. In other cases, it will be due to underwriting appetite of insurers and their ever changing attitudes to risk. Having said that, there are ways you can help yourself.

Their comprehensive approach, combining expert knowledge, personalised service, and a keen attention to detail, has earned them a stellar reputation among policyholders and insurers alike. We look forward to continuing our mission of helping policyholders navigate the complexities of property damage claims with confidence and ease.”

Opaque, ill-defined language empowers predatory “ billboard attorneys ” to define these terms themselves, contributing to pervasive policyholder distrust, said Jeff Sauls, Farmers Insurance head of legislative affairs. Clear communication is key, the participants agreed. Preventing adversaries to the U.S.

points from 2021, according to actuaries at Triple-I and Milliman , a risk-management, benefits, and technology firm. Combined ratio represents the difference between claims and expenses paid and premiums collected by insurers. We forecast 2022 P&C premium growth of 8.5 for 2022, up 1.2 percent,” Porfilio said.

The notion of business coverage can be traced back to medieval times, when the shipping industry first implemented rudimentary forms of risk management. With rapid advancements in machinery and transportation, businesses faced new categories of risk. By the 20th century, the insurance industry began to reflect broader societal shifts.

Businesses may end up with inaccurate ITV calculations for a wide range of reasons — whether it stems from ineffective property valuation methods, intentionally underestimating costs to secure reduced premiums or being impacted by factors outside their control (e.g., They will help determine your risks and advise how to cover them.

The Role of Agents Agents and brokers can help explain these pressures to policyholders who are concerned with rates or repair costs. Another helpful tip for policyholders is to educate them about ways to manage and mitigate their individual risks.

Some digital solutions that may appeal to millennials include usage-based insurance , which allows the policyholder more control over their premium based on driving habits measured through telematics. They can explain how premiums are determined, how policyholders can mitigate their risk, and why certain coverages are important.

Standard home insurance policies may not provide adequate protection for the unique risks associated with a block of flats. When selecting an insurance policy, factors such as the type of tenants, unoccupied flats, and the risk of water leaks and subsidence should be taken into account. What is Block of Flats Insurance?

“The aim of Zywave’s Cyber Quoting is to help the market to grow cyber premium,” said Zywave Senior Vice President Jeff Cohen. “Now, it’s not only faster, but it’s also smarter. ” The Cyber Quoting benchmarking and limit adequacy insights are powered by Zywave’s Commercial Analytics data.

In this article HealthCare.gov policyholders at risk Scammers circumvent consumers protections The damage to affected Marketplace buyers Factors that led to the alleged fraudulent activity Buyers with lower incomes targeted Is this happening in states that run their own Marketplaces? What should consumers do?

It’s a double play—claims processed swiftly, premiums collected seamlessly, and customers satisfied. When a policyholder feels heard, when a claim is resolved swiftly, when premiums align with value—those are the grand slams insurers aim for. The ball never hits the dirt. As the MLB season heats up, keep an eye on Majesco.

This might seem like an advantage since this saves cost initially, though it might lead to high premium costs later on. These can be added to your policy for an additional premium. If your property is located in an area with a high risk of natural disasters, such as floods or earthquakes, your insurance premiums will be higher.

Surety’s Defenses : The surety may invoke certain defenses against the obligee’s claim, such as contract modifications that increase the surety’s risk without consent or the obligee’s failure to comply with contractual conditions that mitigate the surety’s obligations.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content