This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The higher the risk, the higher the workerscompensation premium for that classification. These rules are established by rating organizations like the National Council on Compensation Insurance (NCCI) in most states, though some states have their own rating bureaus. All state laws vary.

By understanding the role fear plays in workerscompensation claims, employers can implement strategies to foster trust, improve outcomes, and reduce costs. The Link Between Fear and Litigation Studies have consistently identified fear as a major driver of workerscompensation litigation. All state laws vary.

Many companies operate under an unwritten rule: accept every workerscompensation claim, no questions asked. A well-managed workerscompensation program should pay 100% of legitimate claimsand 0% of the claims that arent. You should consult with your insurance broker, attorney, or qualified professional.

The ultimate beneficiaries are the injured workers who experience improved care and quicker reintegration into their professional and personal lives. He is co-author of the #1 selling comprehensive training guide Your Ultimate Guide to Mastering Workers Comp Costs: Reduce Costs 20% to 50%. All state laws vary.

Evidence-Based Medicine (EBM) plays a critical role in workerscompensation, guiding both medical professionals and non-medical stakeholders in making informed decisions about injury treatment, recovery time, and return-to-work strategies. You should consult with your insurance broker, attorney, or qualified professional.

By demystifying EBM, workers’ compensation stakeholders are better equipped to provide effective, informed care that facilitates quicker recovery and improved cost management. He is co-author of the #1 selling comprehensive training guide Your Ultimate Guide to Mastering Workers Comp Costs: Reduce Costs 20% to 50%.

Related Content: Use A Medical Advisor To Maximize Value of Independent Medical Exam How to Tell If You Need a Nurse Case Manager for Your WorkersCompensation Claim Peer Review & Peer Matching Central Components Of Work Comp Medical Management Make use of a Nurse Case Manager: In complex cases with multiple provider coordination.

It’s been proven across multiple research studies, including landmark work by the WorkersCompensation Research Institute (WCRI). He is co-author of the #1 selling comprehensive training guide Your Ultimate Guide to Mastering Workers Comp Costs: Reduce Costs 20% to 50%. All state laws vary.

Click Link to Access Free PDF Download “Step-By-Step Process To Master Workers Comp In 90 Days” 3. Brokers and Agents: Employer Advocates Brokers serve as intermediaries between employers and insurance companies. You should consult with your insurance broker, attorney, or qualified professional.

The higher the risk, the higher the workers’ compensation premium for that classification. These rules are established by rating organizations like the National Council on Compensation Insurance (NCCI) in most states, though some states have their own rating bureaus. All state laws vary.

Exclusivity: Protection Against Lawsuits One of the most significant benefits of workerscompensation for employers is the exclusive remedy provision. Under this system, employees who accept workerscompensation benefits for a work-related injury or illness forfeit the right to sue their employer for negligence.

At the heart of this process is the medical director, medical department, or consultant, who plays a pivotal role in interpreting medical jargon and facilitating smooth communication between medical professionals, injured employees, and the workers’ compensation team.

This post will dive into the two primary reasons why workers’ compensation costs are often higher than they should be, and how employers can take charge of the process to reduce those expenses. Visit Amaxx Workers’ Comp Training Center for more insights and resources on effective workers’ compensation management.

Consider the case of Jane, a worker who sustained a severe back injury. She was given a list of four medical providers but found that: Two providers did not accept workerscompensation patients. One provider accepted workerscompensation but was not taking new patients. Are currently accepting new patients.

5 Reasons Why Workers’ Compensation Reserves Are Higher Than Expected: 1. Disability Rating Adjustments: If the employee’s disability rating is higher or lower than initially predicted, this will affect the compensation they are entitled to, necessitating a reserve adjustment. Is the Cost for the Claim for Life?

Reduces Workers’ Compensation Costs : Keeping employees engaged in transitional duty roles helps reduce the overall costs associated with workers’ compensation claims. He is co-author of the #1 selling comprehensive training guide “Your Ultimate Guide to Mastering Workers’ Comp Costs: Reduce Costs 20% to 50%.”

The Role of Physical Therapy in Workers’ Compensation Physical therapy plays a significant role in the workers’ compensation process by improving recovery rates and facilitating quicker returns to work. You should consult with your insurance broker, attorney, or qualified professional. All state laws vary.

FREE DOWNLOAD: “Step-By-Step Process To Master Workers’ Comp In 90 Days” Document the Incident All workplace injuries should be properly documented as soon as possible. Proper documentation not only aids in managing the workers’ compensation claim but also helps protect the employer against potential legal challenges.

Michael Stack, CEO of Amaxx LLC, is an expert in workers’ compensation cost containment systems and provides education, training, and consulting to help employers reduce their workers’ compensation costs by 20% to 50%. You should consult with your insurance broker, attorney, or qualified professional.

These metrics are fundamental in determining the experience modification factor (often called “mod”), which ultimately influences the cost an employer will pay for workers’ compensation insurance. Stack is the creator of Injury Management Results (IMR) software and founder of Amaxx Workers’ Comp Training Center.

These employees, known as “general exclusions,” require their payroll to be reported and calculated separately, directly influencing workerscompensation premiums. ” Stay tuned to complete your understanding and gain further control over your workers’ compensation premiums. All state laws vary.

By setting clear criteria for when to use, not use, and stop using NCM, employers can ensure resources are utilized effectively while maintaining optimal outcomes for injured workers. He is co-author of the #1 selling comprehensive training guide Your Ultimate Guide to Mastering Workers Comp Costs: Reduce Costs 20% to 50%.

FREE DOWNLOAD: “13 Research Studies to Prove Value of Return-to-Work Program & Gain Stakeholder Buy-In” Business and Financial Benefits of Transitional Duty Lower WorkersCompensation Costs : Employees who stay engaged at work tend to have shorter claims duration and fewer legal disputes. All state laws vary.

There are elements in your workerscompensation program that may be creating challenges without you even realizing it. Drivers of Human Behavior in WorkersCompensation The science of human behavior has been studied extensively, and one of the most insightful works on the subject is Drive by Daniel Pink.

Click Link to Access Free PDF Download “Step-By-Step Process To Master Workers Comp In 90 Days” Start With Goal of Where You Want to Go We start with a goal of where we want to go. If you’re a service provider, broker care, captive manager, et cetera. Okay, Mr. Senior Manager, this is what we’re working on.

Michael Stack, CEO of Amaxx LLC, is an expert in workers’ compensation cost containment systems and provides education, training, and consulting to help employers reduce their workers’ compensation costs by 20% to 50%. You should consult with your insurance broker, attorney, or qualified professional.

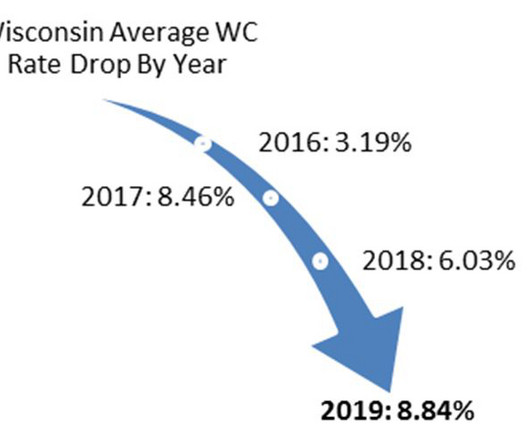

On October 1, 2024 Wisconsin continued its trend entering a ninth consecutive year of reduced workerscompensation insurance rates. Workerscompensation rates are state mandated in Wisconsin, meaning all insurance carriers must use the same rates resulting in premiums from one carrier to another are basically the same.

Revamping a workerscompensation (WC) program can transform how companies manage costs and care for injured employees. Below, we explore common errors and provide actionable steps to begin reforming a workers’ comp program. You should consult with your insurance broker, attorney, or qualified professional.

As the industry evolves, embracing and refining these guidelines will be key to fostering better outcomes and creating a more resilient workers’ compensation system. He is co-author of the #1 selling comprehensive training guide Your Ultimate Guide to Mastering Workers Comp Costs: Reduce Costs 20% to 50%.

Click Link to Access Free PDF Download “Avoid the 3 Primary Reasons Injured Workers Hire Attorneys” Common Communication Gaps Workerscompensation attorneys frequently cite communication breakdowns as the primary reason injured workers seek legal representation. All state laws vary.

In the complex world of workerscompensation, risk managers play a vital role in aligning strategic oversight with day-to-day claims operations. Heres a closer look at best practices every risk manager should be following to create a high-performing, cost-effective workerscompensation program. All state laws vary.

When managing workers’ compensation, a claim audit or review is a crucial opportunity for employers, carriers, TPAs (Third-Party Administrators), and brokers to come together and optimize claim-handling practices. However, this approach is unproductive. Instead of pointing fingers, focus on constructive dialogue.

As a general rule, workerscompensation insurance is the primary insurance, which requires the claim team to investigate and make determinations regarding compensability and subrogation rights. Now is the time to consider these factors to reduce workerscompensation program costs. All state laws vary.

At the same time, companies must navigate various state and federal laws like the Worker Adjustment and Retraining Notification (WARN) Act, which requires advance notice for mass layoffs or plant closures, allowing employees to plan their future employment. You should consult with your insurance broker, attorney, or qualified professional.

Claims Management Oversee the workers’ compensation claims process, ensuring timely filing and follow-up. Michael Stack, CEO of Amaxx LLC, is an expert in workers’ compensation cost containment systems and provides education, training, and consulting to help employers reduce their workers’ compensation costs by 20% to 50%.

Managing workerscompensation can feel like playing whack-a-mole. One day its a delayed report, the next its an escalating claim or a frustrated injured worker. Weekly Claims Roundtables Meet with your claims team (adjuster, broker, internal staff) weekly to discuss open claims. All state laws vary.

By shifting your perspective from compliance-as-burden to compliance-as-advantage, you can leverage OSHA requirements to create a safer, more productive workplace, reduce workerscompensation costs , and enhance your company’s reputation. You should consult with your insurance broker, attorney, or qualified professional.

Michael Stack, CEO of Amaxx LLC, is an expert in workerscompensation cost containment systems and provides education, training, and consulting to help employers reduce their workerscompensation costs by 20% to 50%. You should consult with your insurance broker, attorney, or qualified professional.

Michael Stack, CEO of Amaxx LLC, is an expert in workerscompensation cost containment systems and provides education, training, and consulting to help employers reduce their workerscompensation costs by 20% to 50%. You should consult with your insurance broker, attorney, or qualified professional.

Issues concerning permanent total disability (PTD) benefits are a significant cost driver in workers’ compensation claims. You should consult with your insurance broker, attorney, or qualified professional. This series of articles explores the many aspects of PTD claims and how to deal with them. All state laws vary.

When embarking on the journey to master workerscompensation, the road is well-traveled and marked by proven strategies. Our three components to achieve workers comp mastery are: Framework , Employer Controls , and External Controls. Workerscompensation programs are multifaceted, and leaders often struggle to prioritize.

When a workerscompensation claim spirals into a costly, prolonged, or litigated nightmare, most people instinctively look for a technical failure: late paperwork, a coverage issue, or a misstep by the claims adjuster. The real reason many workers comp claims go off the rails? All state laws vary.

Michael Stack, CEO of Amaxx LLC, is an expert in workerscompensation cost containment systems and provides education, training, and consulting to help employers reduce their workerscompensation costs by 20% to 50%. You should consult with your insurance broker, attorney, or qualified professional.

Assignment of Classification Codes Initially, insurance brokers typically assign classification codes when securing coverage for employers. Brokers discuss the nature of the employer’s work to determine the most suitable code. You should consult with your insurance broker, attorney, or qualified professional.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content