This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In this three-part series, we are examining nine elements of independent premium audits to help you better understand and control your workers’ compensation premiums. These foundational aspects are crucial for ensuring accurate premium calculations and avoiding costly mistakes.

When an employer receives a revised workers’ compensation premium bill, the accuracy of the bill can be uncertain and confusing. To ensure fairness and correctness, an independent premium audit is highly recommended. Payroll Information A critical step in any premium audit is the review of an employer’s payroll.

In this final part of our series exploring the nine elements of independent premium audits, we turn our focus to specialized situations and nuanced adjustments auditors carefully evaluate. Auditors disallow estimates, making precise documentation vital to receiving the intended premium savings associated with this exception.

Many companies operate under an unwritten rule: accept every workers compensation claim, no questions asked. A well-managed workers compensation program should pay 100% of legitimate claimsand 0% of the claims that arent. Employees come to believe that every claim will be accepted, regardless of the circumstances.

As an insurancebroker, you can be the compass your clients need. Key Takeaways : Brokers should stay informed to empower their clients. Brokers should advocate for clients year-round, assisting with claims and policy updates. This means assisting with any claims issues and answering coverage questions.

These rules not only influence the amount you pay in premiums but also help ensure that your company is correctly classified based on the work it performs. Misclassification can lead to costly errors, either by overpaying premiums or by facing penalties for underreporting risk. What Are Classification Rules?

When it comes to calculating workers’ compensation premiums, two critical factors play a significant role: the frequency and severity of claims. Understanding how these two factors interact can help businesses reduce their premiums and improve workplace safety.

How a Liability Claim Can Ruin Your Business And How to Protect Yourself No matter how well you run your business, a single liability claim can have devastating consequences. Get a Quote Insurance under one roof We are specialists in many types of insurance GET YOUR QUOTE GET YOUR QUOTE 1.

Effectively managing workers compensation requires careful oversight and proactive measures to identify and prevent fraudulent or exaggerated claims. Surveillance serves as a powerful tool in validating claims, protecting your organizations financial health, and ensuring resources are dedicated to genuinely injured employees.

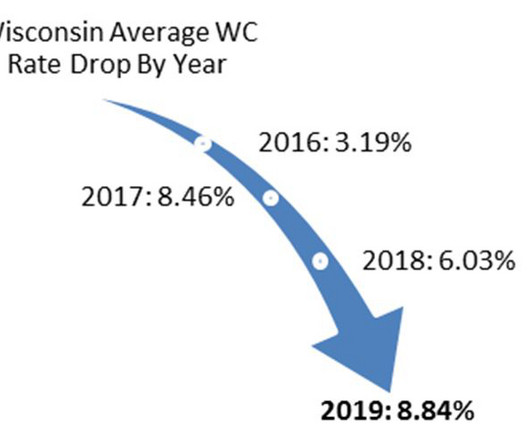

Workers compensation rates are state mandated in Wisconsin, meaning all insurance carriers must use the same rates resulting in premiums from one carrier to another are basically the same. the Good In general, a reduction of work comp rates result in reduced premium costs to contractors. HVAC Installation -14.6 Landscaping -6.3%

These resources are invaluable for both property owners and insurancebrokers when assessing risk. How do pending or unresolved housing violations affect a property owners ability to obtain insurance? Insurers view these violations as signs of deferred maintenance and increased risk.

A medical health insurancebroker helps you choose the best health insurance plan tailored to your needs. Unlike agents tied to one insurer, brokers work with multiple companies to give you unbiased options. What is a medical health insurancebroker?

This diversity in building age and structure affects insuranceolder buildings may face higher premiums due to maintenance risks, while newer developments may require higher coverage for cutting-edge amenities. Insurers view these uses as higher risk, which can lead to increased premiums or the need for specialist insurance policies.

As 2024 unfolds, the Directors and Officers (D&O) Insurance market is hitting yet another turning point. After several years of dramatic rate fluctuations, insurers, brokers, and businesses are bracing for what could be a defining year for D&O premiums. According to Woodruff Sawyer , one of the largest U.S.-based

These rules not only influence the amount you pay in premiums but also help ensure that your company is correctly classified based on the work it performs. Misclassification can lead to costly errors, either by overpaying premiums or by facing penalties for underreporting risk. What Are Classification Rules?

The trajectory of average D&O Insurancepremiums has been a critical barometer for Cyber Insurancebrokers keen on gauging the market’s pulse. After a tumultuous 2021 , the horizon seemed promising as brokers witnessed a stabilization of D&O pricing in 2022.

Predictability in Costs Workers compensation insurance can transfer a portion of the financial risk associated with workplace injuries to the insurance company. Employers pay premiums for this coverage, enabling them to forecast and plan for these costs more effectively.

Insurers view these violations as signs of deferred maintenance and increased risk. Even if some violations are eventually addressed, a history of non-compliance can still lead to higher premiums. Landlord insurance which covers both liability and property damageis particularly sensitive to housing violations.

Insurers view these violations as signs of deferred maintenance and increased risk. Even if some violations are eventually addressed, a history of non-compliance can still lead to higher premiums. Are there specific types of insurance that are more sensitive to these housing violations?

Navigating workers’ compensation can be complex, with various parties working together to ensure effective claims management and cost containment. They are a vital entity, as they not only handle premium collections but also pay out claims to cover medical expenses and wage replacement for injured employees.

But there will also be the same sort of changes that enrollees see every year, in terms of adjustments to plan designs, provider networks, and premiums – including changes to subsidy amounts that can affect net premiums. Premium tax credit eligibility is governed by IRS rules that are applicable nationwide.

Higher Property Values and Rebuild Costs London property prices are significantly higher than the national average, which means higher rebuild costs and, consequently, higher insurancepremiums. Many insurers require more detailed valuations and risk assessments due to the higher sums insured.

In Chicago, housing code violations not only affect tenant safety and property values but also play a critical role in insurance risk assessments. Understanding these violationsfrom heating failures to structural hazardsis essential for insurancebrokers advising property owners. Insurancebrokers are pivotal in this arena.

Or you might have opted to buy ACA-compliant coverage outside the exchange , if you weren’t eligible for premium tax credits (subsidies) the last time you looked. In addition to being more widely available, premium subsidies are also larger than they were before the American Rescue Plan. Letting your plan auto-renew?

Our Claims Partner, Aspray, Wins Loss Assessor of the Year 2024 We are delighted but not surprised to announce that our claims partner, Aspray, has won the prestigious “Loss Assessor of the Year 2024” award at the British Claims Awards.

The direct costs of workers’ compensation claims, medical expenses, and lost productivity add up quickly. Data from OSHA and the National Safety Council consistently show that businesses that invest in safety programs experience lower insurancepremiums, fewer lost workdays, and improved productivity. Heres how: 1.

We work closely with our Insurers to get the best rates and our experience and excellent relationships with them mean that we can provide cover for even the most difficult to place risks. Whether you have an adverse claims history, a high value property or a large portfolio of properties, we can source suitable cover for you.

However, for insurancebrokers, the wide spectrum of restaurants represents both a challenge and an opportunity. With thousands of restaurants in Charlotte and across North Carolina, the need for comprehensive insurance coverage is vital.

We work closely with our Insurers to get the best rates and our experience and excellent relationships with them mean that we can provide cover for even the most difficult to place risks. Whether you have an adverse claims history, a high value property or a large portfolio of properties, we can source suitable cover for you.

Click Link to Access Free PDF Download “How to Calculate Your Minimum Experience Mod, Controllable Premium & the Revenue Impact” Things that we don’t understand can seem a lot more difficult than they actually are. This is the actual costs of the claims that were legitimate claims for workers’ compensation.

We work closely with our Insurers to get the best rates and our experience and excellent relationships with them mean that we can provide cover for even the most difficult to place risks. Whether you have an adverse claims history, a high value property or a large portfolio of properties, we can source suitable cover for you.

” If you don’t have the opportunity to check out the full webinar, read on for key insights from the discussion and actionable advice for insurers, brokers, and policyholders. And when you take into consideration that Direct Premiums Written (DPW) increased by 2.0%

In this article, we will provide you with four essential tips to help you understand your coverage needs, find the best rates, review and update your policy regularly, and work with an experienced insurancebroker. Product Liability Insurance As a tailor, you create and sell products to your customers. Let’s dive in!

In New York City, housing code violations challenge property owners, tenants, and insurancebrokers alike. We speak with Katie Vespia, President of Distinguisheds Real Estate program , about common NYC violations, their fines, resolution processes, and the impact on insurance coverage.

How do you make money as an insurance agent? The insurancebroker is able to earn money from commissions when they start selling insurance products to customers. The commissions come from a percentage coming from the amount of the yearly premium, as well as the policy it is being offered for.

Increase Your Deductible Increasing your deductible is one of the simplest ways to lower your insurancepremiums. This means you will pay more out of pocket in case of a claim, but your monthly or annual insurance costs will be lower. Strategy: Install modern fire alarms, sprinkler systems, and security systems.

Recent data from 2023 and 2024 highlights the financial strain on insurers and property owners alike, driven by more severe storms, heavy rainfall, and unpredictable weather patterns. Rising Claims Due to Extreme Weather In 2023, UK insurers faced record-breaking claims from weather-related damage.

So this is your premium adjustments, and these are discretionary adjustments that can be given by your underwriter based on how well they perceive you managing your risk, how well they perceive you managing your risk. You’re gonna have to some of these premium adjustments. We’ve got things under control based on your mod.

These are just some of the excuses we hear of from the question of, “ Why can’t I get insurance ?” ” or can’t get the insurance you deserve for that matter – insurance with reasonable premiums and without unnecessary restrictions.

Get a Quote Insurance under one roof We are specialists in many types of insurance GET YOUR QUOTE GET YOUR QUOTE Key Takeaways Consistent rate increases have been experienced in the property insurance market since 2017. Inflation drives up property valuations , construction costs , and insurancepremiums.

. “Understanding Multi-Family Property Insurance” Commercial property insurance is a vital safeguard for property owners, protecting their assets against various risks. It covers property damage, loss of income, liability claims, etc.

Whilst we’re predominantly a commercial insurancebroker, the new ruling affects our high-value household policies. Key changes The new rules have brought some key changes to the way General Insurance works: Equivalent policy premiums should not be higher for existing customers than for new customers. Premium reductions?

In this article, we’ll explain the benefits of using a broker, how to find a reliable one, and key questions you should ask. Key Takeaways Medical insurancebrokers serve as intermediaries, helping clients navigate the insurance market and find suitable health plans tailored to their unique needs.

This might seem like an advantage since this saves cost initially, though it might lead to high premium costs later on. Define the maximum amount that you are willing to spend additional in the case of a claim. It is important not to rely only on the words that a broker tells you, try to read all the details.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content