This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A manufacturer and its workerscompensationinsurer thought an injured 60-year old service technician employee did not work hard enough to find a suitable replacement job as required to qualify for wage loss benefits. Among other things, he did not …

The impact and surge of long-term COVID on the California workers’ compensation system since 2020 has been prevalent, including long-term impacts on disability and long-term patterns of medical cost and treatment on long COVID claims. That’s from a report by …

Exclusivity: Protection Against Lawsuits One of the most significant benefits of workerscompensation for employers is the exclusive remedy provision. Under this system, employees who accept workerscompensation benefits for a work-related injury or illness forfeit the right to sue their employer for negligence.

Claim frequency in California workers’ compensation remains significantly higher in the Los Angeles Basin than in the northern part of the state, a new study shows. The Workers’ CompensationInsurance Rating Bureau of California released its WCIRB Geo Study 2024, …

When it comes to calculating workers’ compensation premiums, two critical factors play a significant role: the frequency and severity of claims. Frequency: The Stronger Driver of Premiums In the world of workers’ compensation, frequency refers to how often claims are filed.

Rassp, Presiding Judge, WCAB Los Angeles, California Division of Workers’ Compensation Disclaimer: The material and any opinions contained in this article are solely those of the authors and are not the opinions of the Department of Industrial Relations, Division of Workers’ Compensation, or the WCAB, or any other entity or individual.

As a general rule, workerscompensationinsurance is the primary insurance, which requires the claim team to investigate and make determinations regarding compensability and subrogation rights. This requires them to take a crash course in claims investigation literally.

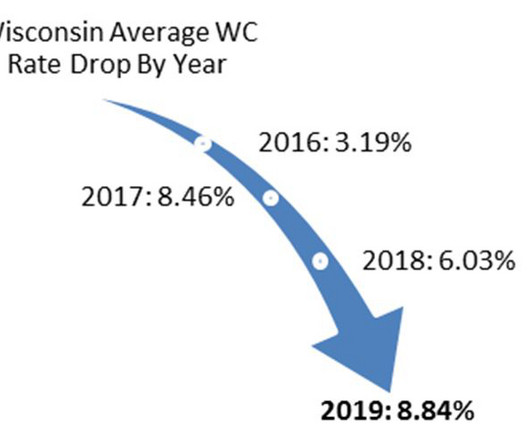

On October 1, 2024 Wisconsin continued its trend entering a ninth consecutive year of reduced workerscompensationinsurance rates. Workerscompensation rates are state mandated in Wisconsin, meaning all insurance carriers must use the same rates resulting in premiums from one carrier to another are basically the same.

Commercial Liability Insurance to protect against claims related to third-party injuries or property damage. WorkersCompensationInsurance to cover employee injuries on the job. If youre hiring new employees at your new location, ensure compliance with local workers comp laws.

By William Nibbelin, Senior Research Actuary, Triple-I The workerscompensationinsurance industry experienced its second-best underwriting result in the past 20 years in 2023, with a net combined ratio of 87, according to Triple-Is latest Issues Brief. A combined ratio under 100 indicates a profit. percent from 2014 to 2023.

COMPLEX EMPLOYMENT ISSUES FOR CALIFORNIA WORKERS' COMPENSATION A new softbound supplement to Rassp & Herlick, California Workers’ Compensation Law 284 pages PIN #0006801214509 For current pricing and to order, call 800-543-6862. What constitutes an independent contractor?

By Julius Young, Richard Jacobsmeyer, Barry Bloom, Editors-in-Chief for Herlick, California Workers’ Compensation Handbook [Note: This article is excerpted from the upcoming 2025 edition of Herlick, California Workers’ Compensation Handbook. The AI revolution is starting to come to workers’ compensation.

All businesses with workers in California and Nevada are required to have WorkersCompensationInsurance. But do you know that Word & Browns partnership with CompNet Insurance Solutions makes it easy for you to offer Workers Comp coverage? What Is Workers Comp? Nevada followed in 1913.

Robinson, Co-Editor-in-Chief, Workers’ Compensation Emerging Issues Analysis ( LexisNexis ) (This article is excerpted from the upcoming 2024 Edition of Workers’ Compensation Emerging Issues Analysis (LexisNexis). By Thomas A. Section numbers below refer to the text in that book. In § 3, Hon.

In New Jersey, the WorkersCompensation Act is the exclusive remedy for injured workers as stated in N.J.S.A. A very recent Supreme Court decision squarely addressed the question whether an insurer is required to defend an employer against intentional harm claims. In Laidlow v. Hariton Machinery Co.,

California workers’ compensation written premium in 2023 was slightly above 2022, while written premium for the first six months of 2024 is 2% lower than the first six months of 2023, a new report shows. The Workers’ CompensationInsurance Rating …

The California workers’ compensation system has been relatively stable in the post-pandemic era, as premium levels rose by 1% in 2023 and are forecast to increase modestly in 2024—while decreases in average insurer charged rates are moderating, a new report …

Professional Liability Insurance (Errors & Omissions Insurance) For IT consultants, developers, or tech startups, mistakes can happen. Professional Liability Insurance protects your business against claims of negligence, errors, or omissions that result in financial losses for your clients.

Workerscompensationinsurance provides for the cost of medical care, rehabilitation, and wage replacement for injured workers and death benefits for the dependents of persons killed in work-related accidents. Combined ratio represents the difference between claims and expenses paid and premiums collected by insurers.

Claimant fraud and premium fraud are two of the most well-known types of workerscompensation fraud. In these cases, a worker may intentionally fake an injury (claimant fraud) or a business owner may misrepresent their employee headcount or incorrectly classify employees to obtain lower insurance premiums.

Reflect on: – How much you can comfortably allocate from your business budget for insurance premiums. – Potential deductibles and what’s financially viable if you need to make a claim. It’s like finding a sweet spot—insurance that doesn’t overspend your resources but still offers peace of mind.

Solakyan Workers’ CompensationInsurance Fraud—Honest-Services Mail Fraud and Health-Care Fraud—Restitution—U.S. Lexis+ Online Subscribers: You can link to your account on Lexis+ to read the complete headnotes and court decisions, en banc decisions, writ denied summaries, panel decisions and IMR decisions.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content