This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In this guide, we break down the key coverages every apartment building owner needs, highlight common claims, and show you how to offer tailored solutions that keep your clients protected in an ever-changing market. Earthquake and flood coverage : Provides protection for damage to the building and common areas caused by earthquakes or floods.

Distinguisheds coverage options, cost factors, and tailored solutions are designed to protect Chicagos property owners. What Distinguished’s Landlord Insurance Programs Cover in Chicago Our City Insurance program provides robust protection, covering: Property insurance: Covers fires, storms, vandalism, and tenant-related damage.

Protecting these assets in the state requires specialized insurance solutions considering earthquake and wildfire risks. Coverage is offered as an optional add-on, with rates determined by sophisticated modeling that considers location, fragility of items, value of collectibles, storage, deductibles, and other factors.

Protecting these assets in the state requires specialized insurance solutions considering earthquake and wildfire risks. Coverage is offered as an optional add-on, with rates determined by sophisticated modeling that considers location, fragility of items, value of collectibles, storage, deductibles, and other factors.

But with value comes risk, and standard homeowner insurance policies frequently fall short when it comes to protecting one-of-a-kind instruments. Whether a client owns a single expensive guitar or an extensive and varied collection that includes guitars, this coverage provides comprehensive protection that adapts to their unique needs.

Many industries are feeling the uncertainty of tariffs and changing trade policies, which can make underwriting more challenging and pricing less certain. This could cause higher rates in commercial property and homeowners lines. This could create the need for frequent rate changes, adding to consumer uncertainty.

What are some of the key factors you consider when determining appropriate coverage limits and deductibles? If we are comfortable with our exposure, we may consider increasing the AOP deductible and the theft deductible , depending on the underwriting analysis. So specific to limits, I just mentioned security.

At Distinguished, we understand that protecting public art requires specialized coverage tailored to its unique exposures. One of the key reasons is lower deductibles, expert knowledge, and tailored coverage options specifically designed for the unique risks faced by public art installations. How Much Does Public Art Insurance Cost?

With the proper knowledge and expertise, you can help protect your clients’ personal and corporate assets, attract top talent to their boards, and ensure compliance with contractual requirements. This coverage ensures that they are protected even if the company is unable to fulfill its indemnification obligations.

With the proper knowledge and expertise, you can help protect your clients’ personal and corporate assets, attract top talent to their boards, and ensure compliance with contractual requirements. This coverage ensures that they are protected even if the company is unable to fulfill its indemnification obligations.

Discover how inland marine insurance protects businesses with mobile assets, the industries that benefit the most, and how brokers can leverage this coverage to support their clients while expanding their book of business. Businesses with mobile property whether equipment, materials, or cargo need protection beyond standard policies.

Generally, these policies have higher deductibles than standard policies – $25k, $50k, or $100k are common deductibles. Underwriting is extensive and involves separate applications/questionnaires and an extensive review of historical claims.

Key Highlights Comparing Medicare Supplement Plans Insurance, or Medigap, helps cover costs that Original Medicare doesn’t, like copays and deductibles. These plans also help cover coinsurance and hospital costs that Original Medicare does not fully pay for, providing additional financial protection.

Understanding this connection can help you make informed decisions about your investments and protect your financial well-being. Changes in Underwriting Processes Interest rates can also shape the underwriting processes used by insurance companies. Let’s dive into how these changes could affect you.

Designed specifically for the needs of collectors, this specialized coverage offers protection tailored to the high values and distinct risks associated with collectible items. For example, transit coverage , which protects items while they are being shipped or moved, is often excluded from homeowner’s policies.

Are insurers ready to capitalize on the impact of todays customer tipping points at the same time they protect the customer relationships? Hence, every area can take advantage of its features from product development to customer engagement to underwriting, billing, and claims.

TGS Insurance » Blog With hurricane season in full force, South Carolina residents living on the coast must protect their homes from the upcoming storms. Understanding how windstorm insurance works in these areas is the first step in adequately protecting your home. The law protects all land designated “beach” by the legislature.

Investors must understand the importance of securing comprehensive commercial property insurance coverage to protect their investments. “Understanding Multi-Family Property Insurance” Commercial property insurance is a vital safeguard for property owners, protecting their assets against various risks. .

automated deductible and Rx updates (so you know when they apply before benefits kick in). W&Bs Underwriting team works directly with carriers to streamline approvals. Well help you protect your clients from liability and hefty financial penalties in connection with Affordable Care Act (ACA) annual reporting.

The Obligee : Usually the project owner or developer requiring the bond as a form of financial protection against the principal’s non-performance. The surety’s role is complex, as it must diligently assess the risks associated with underwriting bonds. Performance and payment bonds become crucial in managing these risks.

This isn’t the first time the act – which would protect banks from federal penalties for doing business with cannabis-related businesses that comply with state laws – has made it through the House. It was first introduced in March 2019, and the House has approved it three times, only to have the Senate Banking Committee block its progress.

i] The impact on insurers financial results and the growing protection gap for insureds are both unsustainable. The increase in cost for insurance is widening insurance protection gaps which ultimately is not good or sustainable for customers or the industry. The result a growing protection gap for insureds.

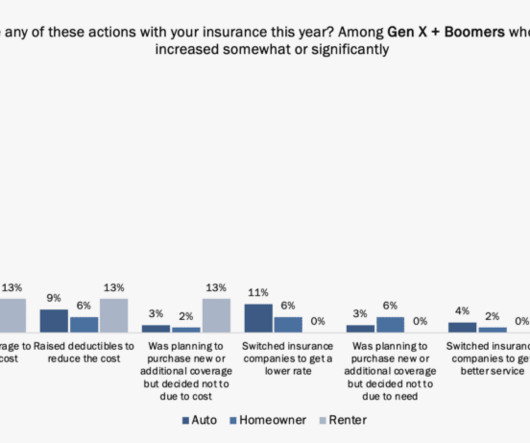

Anything from quoting to underwriting, servicing, billing or claims may no longer operate at the level expected by customers, putting trust and loyalty at risk. In addition, other actions taken included raising deductibles, particularly for homeowners, and reducing coverage for both auto and homeowners.

There is an increasing protection gap for our customers. If we don’t get down to addressing the loss ratio — underwriting, pricing, risk selection, and claims management — for many carriers, even if they cut costs by 100%, they’re still not going to be profitable. We have challenges from a macroeconomic perspective.

Whether your client owns a single high-value decoy or an extensive collection, youll walk away with the knowledge to confidently provide them with specialized coverage that protects their prized possessions. Comprehensive coverage ensures each decoy is protected at its full worth.

With the proper knowledge and expertise, you can help protect your clients’ personal and corporate assets, attract top talent to their boards, and ensure compliance with contractual requirements. This coverage ensures that they are protected even if the company is unable to fulfill its indemnification obligations.

The ACA protects people with pre-existing health conditions. Small businesses and their employees are no longer subject to medical underwriting for health insurance. The ACA requires marketplace plans to cover at least one drug in each drug class and to include out-of-pocket Rx expenses in an insured persons or familys deductible.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content