This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Privilege Underwriters Reciprocal Exchange (2024 WL 322297 (Tex. The insurer paid only a portion of the claim because it maintained that the tornado that struck and damaged the property was a “windstorm” and, therefore, the claim was subject to the policy’s “Windstorm or Hail Deductible.” In Mankoff v. Dallas Jan. Loss of Use.

However, with opportunity comes risk: property damage, liability claims, and unexpected financial losses can quickly turn a profitable investment into a costly liability. Properties near major rivers also face flooding risks. Umbrella insurance offers additional protection to cover unexpected legal and financial risks.

So this is your premium adjustments, and these are discretionary adjustments that can be given by your underwriter based on how well they perceive you managing your risk, how well they perceive you managing your risk. and why are we gonna try to get this risk up because you’re saying, hey. Say that again.

We sat down with Distinguished’s Builder’s Risk insurance expert, Susan DeCarlo, to discuss common factors that can lead to declinations in our program, how to avoid them, and key risk considerations. So, for example, on a new build if they’re 30 to 60 days in, we can consider that risk.

Many industries are feeling the uncertainty of tariffs and changing trade policies, which can make underwriting more challenging and pricing less certain. At the same time, agents can work with their policyholders to improve risk management and loss control to make the account as attractive as possible when shopping for coverage.

And with rising property values, more frequent catastrophic weather events, and emerging risks like habitability claims, its never been more critical to help your clients navigate their insurance options. Without the right coverage, property owners could be exposed to significant financial and legal risks.

But with value comes risk, and standard homeowner insurance policies frequently fall short when it comes to protecting one-of-a-kind instruments. Transit-related risks : Whether traveling for appraisals, exhibitions, or repairs, rare guitars face an increased risk of loss, theft, or damage and many policies wont cover transit losses.

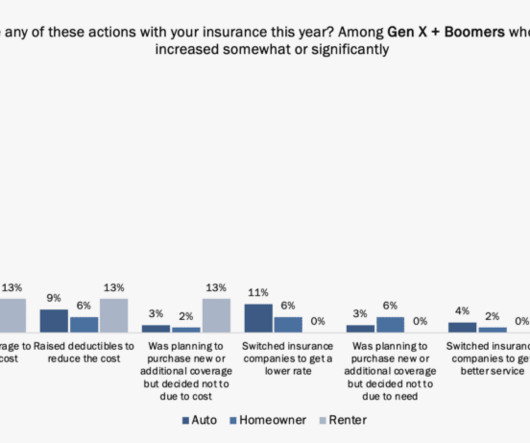

The traditional insurance customer relationship is being re-examined and, in some cases, re-energized by the need to address higher risk and higher premiums. The tipping point mindset shift a toehold for insurers in a disrupted market. From a demographic perspective, it is helpful to track Gen Z/Millennials against Gen X/Boomers.

Risk Management Considerations There are many factors that come into play when considering the environmental conditions that lead to the growth of mold. The primary area where there is opportunity to implement proactive risk management practices is related to moisture.

Protecting these assets in the state requires specialized insurance solutions considering earthquake and wildfire risks. Our program provides all-risk worldwide coverage for direct physical damage like fire and theft of personal collections of any size.

Spotting problem areas and opportunities sooner makes it easier to develop and implement steps to reduce risk pre-loss and better control costs post-loss. This often includes the risk manager, and may also encompass employees from legal, human resources, safety, operations and even the CFO, in some cases.

Protecting these assets in the state requires specialized insurance solutions considering earthquake and wildfire risks. Our program provides all-risk worldwide coverage for direct physical damage like fire and theft of personal collections of any size.

In 2018, the 5 th Circuit Court of Appeals took things a step further in Certain Underwriters at Lloyd’s of London v. Depending on the amount of your deductible, this means recovery could be impossible as a practical matter. Lowen Valley View, L.L.C.

Without legislative change, banks and insurers can’t do business with business without risking running afoul of federal drug laws. The CLAIM Act would let these businesses obtain insurance to cover the same risks of theft, damage, injury, loss, and liability as all other businesses.

However, they also face unique risks, from vandalism and weather damage to transport and installation challenges. One of the key reasons is lower deductibles, expert knowledge, and tailored coverage options specifically designed for the unique risks faced by public art installations. How Much Does Public Art Insurance Cost?

In this brokers guide, we’ll explore what management liability insurance covers, why clients need it, the exposures that go into evaluating a risk, and the benefits of partnering with Distinguished. The cost of Management Liability Insurance is highly dependent on your clients specific risks and characteristics.

In this brokers guide, we’ll explore what management liability insurance covers, why clients need it, the exposures that go into evaluating a risk, and the benefits of partnering with Distinguished. The cost of Management Liability Insurance is highly dependent on your clients specific risks and characteristics.

Changes in Underwriting Processes Interest rates can also shape the underwriting processes used by insurance companies. Underwriting involves evaluating risks and determining suitable premiums for policyholders. Moreover, alongside higher premiums, you may encounter an increase in out-of-pocket costs, such as deductibles.

However, the very qualities that make collectibles so precious also expose them to unique risks. Unfortunately, these unique risks are rarely appropriately covered by standard homeowner insurance policies. We understand the unique risks and how to best insure these special items. For most, this will mean a collectibles policy.

Nationwide, Cincinnati, State Auto, Liberty Mutual, Acuity, Auto Owners, EMC, Grand River, Travelers, Hartford, and Chubb cited heightened risks with call-for-aid systems and will not write insurance to cover any affordable housing elderly communities with installed pull cords.

So, from an insurer’s perspective, your credit score provides a glimpse into potential risk. Increase Your Deductible: Opt for a higher deductible to lower your monthly premium. Upgrade Your Home: Adding safety features like a security system or fire-resistant materials can reduce risk—and your rate. In most cases, yes.

However, with great opportunities come great risks. “Understanding Multi-Family Property Insurance” Commercial property insurance is a vital safeguard for property owners, protecting their assets against various risks. It protects against perils like fire, explosions, storms, and other risks outlined in the policy.

The South Carolina Wind and Hail Underwriting Association, also known as Wind Pool, is an association of insurance providers. The South Carolina Legislature required insurance to be available to at-risk coastal homes. The South Carolina Wind and Hail Underwriting Association has an eligibility checker.

Surety’s Defenses : The surety may invoke certain defenses against the obligee’s claim, such as contract modifications that increase the surety’s risk without consent or the obligee’s failure to comply with contractual conditions that mitigate the surety’s obligations.

Anything from quoting to underwriting, servicing, billing or claims may no longer operate at the level expected by customers, putting trust and loyalty at risk. In addition, other actions taken included raising deductibles, particularly for homeowners, and reducing coverage for both auto and homeowners.

Risk resilience, a key topic for an industry grappling with growing and intensifying risk, is more important than ever. Risk is changing and intensifying. At just the time when insurance purchase and use should be growing due to increased risk, it is underutilized because of perceived affordability issues.

They are looking at their financials, growth, profitability, pace of technology change, increasing risk, and customer demands to determine next steps with their technology foundation. There are some positive things that emerged during 2023 regarding risk prevention. We have to prevent more risk from occurring.

This kind of coverage ensures each piece is protected at its full appraised value and accounts for risks unique to collectible decoys, such as accidental damage, theft, and environmental factors like humidity and warping. A standard homeowner’s or renter’s policy isnt enough.

In this brokers guide, we’ll explore what management liability insurance covers, why clients need it, the exposures that go into evaluating a risk, and the benefits of partnering with Distinguished. The cost of Management Liability Insurance is highly dependent on your clients specific risks and characteristics.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content