This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

property/casualty insurance industry recorded a net underwriting gain of $3.7 “After years of consistent losses, premium growth is helping the overall … billion and net income of $94.6 billion for the first-half of 2024, according to a new report.

Growth in net earned premiums outpaced a slight increase in losses and loss adjustment expenses to result in the U.S. property/casualty industry posting a nine-month 2024 underwriting profit of $4.1 billion versus a loss of $32.1 billion last year. According …

North Carolina Insurance Commissioner Mike Causey is reminding property insurers to refrain from raising homeowners’ premiums just because an insured filed a claim or inquiry in order to qualify for flood insurance indemnity or federal assistance. In most cases, the …

property/casualty insurance industry recorded a net underwriting gain of $3.7 “After years of consistent losses, premium growth is helping the overall … billion and net income of $94.6 billion for the first-half of 2024, according to a new report.

Treaty reinsurance written in the London company market grew by almost one-third in 2023, with the sector generating premiums of £10.889 billion (US$14.2 billion) in 2022, according to the International Underwriting Association (IUA). billion), up from £8.248 billion ($10.8 The …

billion compared to net income of $454 million during the same period a year ago on record net premiums, favorable prior year reserve development, and higher investment income. Travelers on Thursday said third quarter net income was $1.26 The New …

Favorable first-quarter economic and underwriting results for property/casualty insurance are in line with projections that the industry will see a small underwriting loss in 2024 and achieve profitability in 2025, according to a report from the Insurance Information Institute (Triple-I) …

Insurance Carriers are reducing their appetite for risk and increasing premiums. This post is part of a series sponsored by TSIB. This means they are being much more selective in what they are willing to insure. If they are going …

reported second quarter net income of $534 million, compared to a loss of $14 million during the same time a year ago, thanks to record net premiums of about $11.1 The Travelers Companies, Inc. The New York-based insurer posted …

The “gap is closing” between commercial lines and personal lines underwriting results as the insurance industry overall is expected to continue its run of premium growth and improved underwriting results over the next 2 years. According to a report from …

premium growth while maintaining underwriting discipline. The Lloyd’s executives said the market has continued to demonstrate its value to stakeholders by delivering 6.5% Lloyd’s saw a continuation of positive returns with profit before tax of 9.6 billion ($12.4 billion) during …

Commercial auto insurance has struggled to achieve underwriting profitability, even before inflationary conditions affected property/casualty lines in recent years. The trend has been accompanied by steady growth in net written premiums (NWP), according to the Insurance Information Institute (Triple-I), an …

Despite targeted underwriting initiatives, including raising premiums to match the rising … After the U.S. commercial auto insurance segment sustained a $5 billion net loss in 2023, a new AM Best reports indicates further deterioration in the first half of 2024.

Insurance industry rating analysts from AM Best warn recent softer pricing for directors and officers coverage could begin to affect insurers’ underwriting results. AM Best noted renewal premium for monoline D&O liability continued to fall during the first three months …

Commercial auto insurance has struggled to achieve underwriting profitability, even before inflationary conditions affected property/casualty lines in recent years. The trend has been accompanied by steady growth in net written premiums (NWP), according to the Insurance Information Institute (Triple-I), an …

In this final part of our series exploring the nine elements of independent premium audits, we turn our focus to specialized situations and nuanced adjustments auditors carefully evaluate. Auditors disallow estimates, making precise documentation vital to receiving the intended premium savings associated with this exception.

As insurers look to 2025, several trends are emerging that affect premium and deductible costs — leading to lengthy conversations between insurance agents and brokers and their customers. For worship facilities, some of the most prevalent trends include: • Weather-related …

The overall industry’s underwriting results were profitable. The 2024 combined ratio losses and expenses divided by premium, … Armchair analysts prognosticating the impending collapse of property & casualty insurance companies were proven wrong by recently released 2024 financial performance results.

By William Nibbelin, Senior Research Actuary, Triple-I The workers compensation insurance industry experienced its second-best underwriting result in the past 20 years in 2023, with a net combined ratio of 87, according to Triple-Is latest Issues Brief. A combined ratio under 100 indicates a profit. A ratio above 100 indicates a loss.

D&O Dampening “Despite recently favorable statutory underwriting results, the softer pricing of the past couple of years could ultimately dampen the financial performance of D&O insurers because the premium base to support future claims activity has diminished, even as risks …

property and casualty insurance industry experienced better-than-expected economic and underwriting results in the first half of 2024, according to the latest forecasting report by Triple-I and Milliman. Much of the overall underwriting gain was due to growth in personal lines net premiums written. represented a 2.3-points

When it comes to calculating workers’ compensation premiums, two critical factors play a significant role: the frequency and severity of claims. Understanding how these two factors interact can help businesses reduce their premiums and improve workplace safety. Underwriters view very large losses as rare and unlikely to repeat.

Despite targeted underwriting initiatives, including raising premiums to match the rising … After the U.S. commercial auto insurance segment sustained a $5 billion net loss in 2023, a new AM Best report indicates further deterioration in the first half of 2024.

The Birthday Rule is gaining traction across the country, allowing Medicare Supplement policyholders to switch plans without medical underwriting around their birthday each year. Reduced underwriting can lead to higher premiums , increased policy lapses, and fewer carriers remaining in the market. in 2024 vs. 13.0%

The commercial auto insurance line has struggled to achieve underwriting profitability for years, even before the inflationary conditions that have been affecting property/casualty lines more recently. This trend has been accompanied by steady growth in net written premiums (NWP).

However, this market comes with its own set of challenges, including price sensitivity, unique underwriting processes, and sometimes, a lack of awareness among consumers. Key products to consider include: Whole Life Insurance : A staple for final expense agents, it provides lifelong coverage at affordable premiums.

TGS Insurance » Blog Homeowners Insurance Underwriting Questions: What to Expect When Getting a Quote So, you’re ready to take the plunge into homeowners insurance. Either way, there’s a step that often surprises people when they go to get a quote—the underwriting process. And, trust me, it can feel a bit like playing 20 Questions.

Rising expenses could perhaps cause higher insured values, leading to policy adjustments and higher premiums. Many industries are feeling the uncertainty of tariffs and changing trade policies, which can make underwriting more challenging and pricing less certain. Education is often the first step.

Insurers are attempting to stem persistent losses on their underwriting The post Home insurance premiums to keep rising in ‘difficult year’ appeared first on Elmore Insurance Brokers.

Insurance companies rely on these reports to assess risk when underwriting a new policy. The most common report is the Comprehensive Loss Underwriting Exchange (C.L.U.E.) If a property has multiple claims, it might lead to: Higher premiums Frequent past claims signal higher risk. Why Should Homebuyers and Homeowners Care?

The property & casualty insurance industry’s combined ratio – an indicator of underwriting profitability – is forecast at 100.7 Combined ratio represents the difference between claims and expenses paid and premiums collected by insurers. We forecast 2022 P&C premium growth of 8.5 for 2022, up 1.2 percent,” Porfilio said.

After several years of dramatic rate fluctuations, insurers, brokers, and businesses are bracing for what could be a defining year for D&O premiums. The D&O Insurance market experienced a favorable underwriting performance in 2023, with the sector seeing its best loss ratio since 2014. With class action settlements totaling $2.1

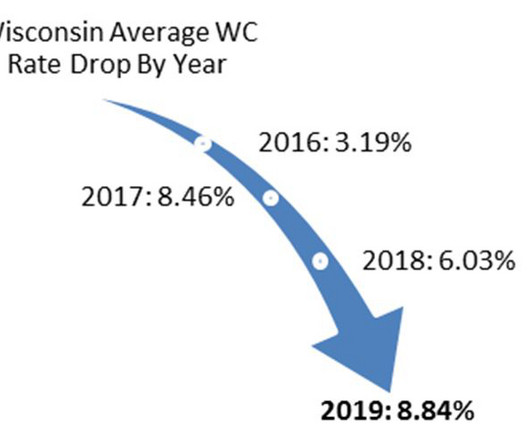

Workers compensation rates are state mandated in Wisconsin, meaning all insurance carriers must use the same rates resulting in premiums from one carrier to another are basically the same. While at first glance, this appears a boon to the bottom line for Wisconsin contractors as work comp premium makes up the lions share of insurance costs.

In Los Angeles, housing code violations present challenges that affect property safety, compliance, and insurance underwriting. Even if some violations are eventually addressed, a history of non-compliance can still lead to higher premiums. Can you outline some of the most common housing violations in Los Angeles?

In two years, he successfully implemented over 20 partnerships with major insurance brokers and significantly enhanced Arch’s digital presence while optimizing the underwriting process through automation, culminating in improved user interfaces and portals.

When our underwriting teams evaluate a new policy, they primarily look at the following three factors to determine pricing: Maintenance : Whether the property is well looked after and is free from any characteristics that would make it more risky or ineligible for coverage. We prioritize human insights over automation.

I was thinking about this because of this article , coincidentally also today, in the Guardian which shows that homeowners premium increases in various parts of the United States align consistently with the extent of that particular part of the countrys increased risk of loss from climate related events.

Claims-related litigation is down, the “ depopulation ” of the state’s insurer of last resort continues apace, and underwriting profitability – while still in negative territory – has improved significantly. One factor keeping upward pressure on rates is fraud and legal system abuse. With only 15 percent of U.S.

Even if some violations are eventually addressed, a history of non-compliance can still lead to higher premiums. Both resolved and unresolved violations can affect the terms, premiums, and overall coverage of these policies. She oversees the programs strategic planning, product management, and underwriting profitability.

The trajectory of average D&O Insurance premiums has been a critical barometer for Cyber Insurance brokers keen on gauging the market’s pulse. This rise in D&O claims is expected to push premiums upward as insurers recalibrate risk assessments.

By Lewis Nibbelin, Guest Blogger for Triple-I Home and auto insurance premium rates have been a topic of considerable public discussion as rising replacement costs and other factors – from climate-related losses to fraud and legal system abuse – have driven rates up and, in some states, crimped availability and affordability of coverage.

When determining the price of a policy, our underwriters will look at factors such as the restaurants size, location, type of services offered, and additional coverage needs. Location risks: Areas with higher crime rates or increased foot traffic face higher premiums.

Zywave’s proprietary data tools are designed to help you improve your underwriting efficiency, refine your rates and better educate policyholders on the risks they may face. That’s where Cyber OverVue comes in.

So this is your premium adjustments, and these are discretionary adjustments that can be given by your underwriter based on how well they perceive you managing your risk, how well they perceive you managing your risk. You’re gonna have to some of these premium adjustments. It’s it’s not showing me that you do.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content