This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

commercial autoinsurance segment sustained a $5 billion net loss in 2023, a new AM Best reports indicates further deterioration in the first half of 2024. Despite targeted underwriting initiatives, including raising premiums to match the rising … After the U.S.

Commercial autoinsurance has struggled to achieve underwriting profitability, even before inflationary conditions affected property/casualty lines in recent years. The trend has been accompanied by steady growth in net written premiums (NWP), according to the Insurance Information Institute (Triple-I), an …

Commercial autoinsurance has struggled to achieve underwriting profitability, even before inflationary conditions affected property/casualty lines in recent years. The trend has been accompanied by steady growth in net written premiums (NWP), according to the Insurance Information Institute (Triple-I), an …

commercial autoinsurance segment sustained a $5 billion net loss in 2023, a new AM Best report indicates further deterioration in the first half of 2024. Despite targeted underwriting initiatives, including raising premiums to match the rising … After the U.S.

Rising expenses could perhaps cause higher insured values, leading to policy adjustments and higher premiums. Many industries are feeling the uncertainty of tariffs and changing trade policies, which can make underwriting more challenging and pricing less certain. Education is often the first step.

Even as California moves to address regulatory obstacles to fair, actuarially sound insuranceunderwriting and pricing, the states risk profile continues to evolve in ways that impede progress, according to the most recent Triple-I Issues Brief.

The commercial autoinsurance line has struggled to achieve underwriting profitability for years, even before the inflationary conditions that have been affecting property/casualty lines more recently. This trend has been accompanied by steady growth in net written premiums (NWP).

property and casualty insurance industry experienced better-than-expected economic and underwriting results in the first half of 2024, according to the latest forecasting report by Triple-I and Milliman. Much of the overall underwriting gain was due to growth in personal lines net premiums written. represented a 2.3-points

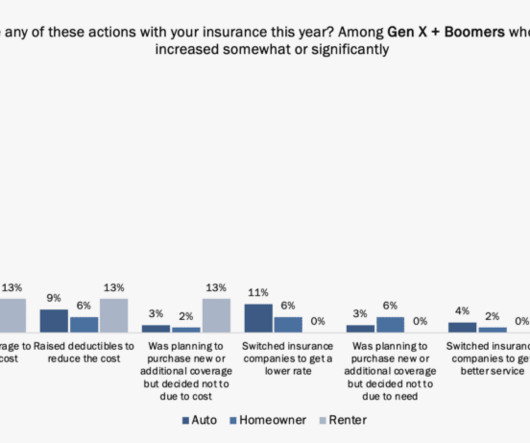

When she recently realized that her premiums for both vehicles were nearly identical (and they had both gone up), she called her insurance agent. The agent suggested a telematics-based insurance product for the convertible to optimize pricing. The potential premium savings are worth the data sharing. They buy differently.

By Lewis Nibbelin, Guest Blogger for Triple-I Home and autoinsurancepremium rates have been a topic of considerable public discussion as rising replacement costs and other factors – from climate-related losses to fraud and legal system abuse – have driven rates up and, in some states, crimped availability and affordability of coverage.

The property & casualty insurance industry’s combined ratio – an indicator of underwriting profitability – is forecast at 100.7 Combined ratio represents the difference between claims and expenses paid and premiums collected by insurers. Losses have been driven by significant deterioration in the personal auto line.

It’s one of those questions that might catch you off guard—after all, what does borrowing history have to do with insuring your home? Let’s explore how and why your credit score affects your home insurance , what insurers are really looking at, and what you can do to keep your premiums manageable. Turns out, quite a bit.

As we’re trying to raise awareness of this problem with consumers, ‘social inflation’ doesn’t work,” said discussion moderator and Triple-I’s Chief Insurance Officer Dale Porfilio. But as the state’s bodily injury claims climb well over the national average, more reform is needed to return insurance profitability to the state.

Does where you live have an impact on how much you pay for car insurance? Surprisingly, it does indeed make a difference where you live when your insurer is determining what you’ll be quoted for your autoinsurance coverage. What Other Factors Determine What I’ll Pay for AutoInsurance?

AI has rapidly transformed the insurance industry and more changes will continue as the technology and use cases mature. New efficient processes and workflows for underwriting, claims, policy administration, billing, and customer service have been implemented across the industry.

[ii] According to the Insurance Journal article, Progressive “outdistanced” GEICO on growth and profitability measures in the first quarter with Progressive reporting a 12% increase in written premiums and a combined ratio of 94.5, points from first-quarter 2021.

Rise of Usage-Based Insurance (UBI) Usage-based insurance models are expected to become more widespread across various insurance lines. Blockchain and Smart Contracts Evolution Blockchain technology and smart contracts will mature to streamline insurance operations and enhance transparency.

Insurers pulled reports and data that were freely available. These were sufficient to improve underwriting or claims. But the good news for insurers and their desire to use AI is that data is important enough now to have a face of its own customers think about it and most customers understand how it improves risk and pricing.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content