This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In a case involving alleged hail damage to a commercial building, the court granted summary judgment in favor of the insurer, Charter Oak Fire Insurance Company, after excluding the policyholder’s expert witness.

At Cowbell, were always looking for innovative ways to help our policyholders improve their risk resilience. Thats why were thrilled to announce the launch of Cowbell Resiliency Services (CRS) , a new suite of cybersecurity solutions designed to proactively enhance the security posture of US-based policyholders.

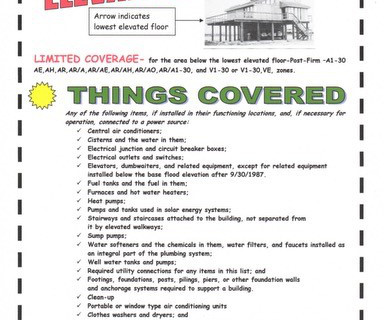

I have received numerous calls from furious Hurricane Helene policyholders after learning how little coverage is afforded for the non-elevated floor of a multi-story building under their flood insurance policies. Refer to the Visual Flood Adjusters Use appeared first on Property Insurance Coverage Law Blog.

A federal judge ruled last week that policyholders eventually have to “put up or shut up” when it comes to proving that certain interior damages caused by a storm must be the result of damage to the exterior of a building, allowing water to damage the interior of a building.

With the launch of Cowbell Resiliency Services (CRS) , were doubling down on that commitment, offering a range of free and subscription-based tools that help our policyholders stay ahead of the ever-evolving threat landscape. The Motivation Behind CRS Why Go Beyond Traditional Cyber Insurance? CRS is the next step in fulfilling that vision.

While the relationship between tariffs and insurance costs can seem unrelated, tariffs can increase costs for insurers and policyholders. Read more to understand this relationship and how agents can help policyholders manage this uncertainty. Here are some ways agents can help: Educate policyholders about costs and rising premiums.

Establishing strong, trusting policyholder relationships drives long-term success for many agents and brokers. Agents and brokers must balance the risk of E&O and policyholder relationships to succeed. Agents can help build trust through transparency and open discussions with policyholders.

With each expansion, we refine our underwriting models in real-time, anchoring our promise to swiftly pay claimsover $250 million disbursed to datewhen policyholders need us most. New Products: Building on a Strong Foundation For five years, Cowbell has refined underwriting precision in cyber and established sweeping distribution channels.

Insurance agents and brokers can also follow this strategy to connect with policyholders. Learn ways to engage with customers and increase policyholder retention by leveraging social media. Policyholders want to work with an agent who understands their needs and educates them on insurance solutions.

Top Building Insurance Pitfalls Here are some common pitfalls to avoid when getting building insurance in the UK: – Underinsuring. Insure your building at the amount that it will cost to rebuild it and not at the current market value when securing block of flats insurance. – Not considering inflation.

We’re prepared to help you grow your distribution network, power your decision making with industry-leading data and insights and empower your teams and policyholders with industry knowledge and expertise. Policyholders are going to experience losses. And your own first-party data isn’t going to get you there.

Flexibility: Medicare supplements allow policyholders to see any doctor or specialist who accepts Medicare, without network restrictions. Build long-term client relationships. Medicare supplements (or Medigap plans) offer: Predictable Costs: Clients appreciate the ability to budget for out-of-pocket healthcare expenses.

Other notable issues include illegal conversions where garages, basements, or other spaces are converted into living areas without proper permitswhich are particularly common in older buildings. After a report is filed, an inspector from the Los Angeles Housing Department or Building and Safety is dispatched to evaluate the situation.

Collaborative partnerships with carriers improve service for policyholders, enhance an agency’s growth potential, and provide learning opportunities for agents. Offer feedback from policyholders and constructive thoughts when interacting with carrier partners. Every relationship is enhanced by clear, open communication.

For buildings constructed before June 13, 1979, strict rent control laws apply. These include unstable buildings, unsafe stairways, or poorly maintained common areas like balconies and porches. Once a report is filed, the Department of Building Inspection (DBI) conducts an inspection. First, there are Rent Control Violations.

If these conditions arent met, the building can be cited for a violation. Structural issues including unstable porches, broken stairs, damaged roofs, or cracked wallscan compromise the safety of a building. A housing inspectorusually from the Department of Buildings (DOB) or Public Healthwill then inspect the property.

This career is deeply rooted in building relationships and providing compassionate service. Myth 5: It’s All About Numbers, Not People While understanding numbers and policies is important, the heart of being a senior benefits agent lies in helping people.

If a buildings indoor temperature falls below the legal minimum, it not only causes discomfort but also attracts fines. Then we have mold and water damage , often stemming from persistent leaks and damp conditions in older buildings. First, there are heating and hot water issues. Another common violation is pest infestations.

For instance, problems with roofs and exterior wallssuch as cracks, leaks, or deteriorating materialscan weaken a buildings overall integrity, while foundation issues like uneven or shifting bases create serious safety hazards. In Philadelphia, housing code violations generally fall into a few key categories.

Policyholders benefit from their agents expertise and knowledge when cross-selling is done well. Learn more about the ethics of cross-selling and how to use it to help policyholders in this blog. It can be a very beneficial practice for agents and policyholders alike when done ethically.

Policyholders are looking for more than just the best rate for their insurance coverage. Agents who position themselves as risk resilience experts can help policyholders become more educated and aware of how to improve their risk exposure and reduce the potential of losses. Conduct personalized risk assessments.

As stories of resilience and courage emerge and the fires are contained, agents and brokers provide critical insurance support for policyholders. For agents serving this challenging market, this means developing a deep understanding of risk and proactive mitigation strategies to assist policyholders before, during, and after a wildfire.

I made similar warnings in Wildfires Leave Dangerous Health Risks In Surviving Buildings. John Putnam wrote an article warning about the dangers of smoke following wildfires, titled, Wildfire Smoke Claims: A Hidden Postwildfire Catastrophe. Putnams article gets right to the point: Where there is fire, there is smoke!

Here are three ways agents can better serve women policyholders: Focus on relationships and positioning yourself as a trusted advisor. An educational, consultative model that builds long-term loyalty may be a better fit. Provide holistic risk management services designed to manage all aspects of a policyholders life.

The homeowners insurance market is complicated and dynamic, and many policyholders have experienced increased rates in recent years despite no changes to their coverage or claims filed. Prices for building supplies, such as lumber, concrete, masonry and steel, have skyrocketed in recent years. Explore discounts. 3 or 5 years).

Agents and brokers play important roles in the digital claims management process, from educating policyholders on loss mitigation to helping insureds file claims and work with their insurers. Knowing how to help these policyholders throughout their claim can be a helpful service agents can offer their insureds.

By understanding key terms, policy details, and the rights and responsibilities of policyholders, consumers can engage with insurers more effectively, ensuring better communication and ultimately achieving their desired outcomes. By exploring these guides, individuals can gain a comprehensive understanding of why insurance is essential.

Market value is based on factors such as lot size, building condition and location desirability. Replacement value depends on factors such as material and labor expenses, architect services, debris removal needs and building permit requirements. dollars per square foot). 80%) of the property’s value. Consult other parties.

Climate change poses an extraordinary challenge for businesses, insurers, and governments alike, making the task of adapting and building resilience feel almost overwhelming. By combining these two approaches, we can tackle the climate challenge head-on and build a future thats both resilient and adaptive.

This innovative approach combines big data, machine learning, and advanced statistical techniques to forecast which policyholders are likely to discontinue their coverage. Acquiring new customers is often more expensive than retaining existing ones, and long-term policyholders tend to be more profitable.

Clear communication enhances understanding, builds trust and reduces mistakes and misunderstandings. Use the data your agency has to build a more complete picture of your customers and prospects and give your agents the ability to craft more creative solutions. Personalize to Build Relationships. Targeted Communications.

He will work directly with the sales, product, and leadership teams to ensure alignment with business objectives, fostering broker and policyholder engagement, and spearheading innovative campaigns that reinforce Cowbell’s position as a leader in cyber insurance. The post Thomas Pytel, Jr.

Today, for insurance agencies, the road from a prospective client to a loyal policyholder can often feel like a winding journey filled with uncertainties. This significant increase highlights the importance of consistent communication and relationship-building in the insurance industry.

We remain steadfast in our commitment to fostering market innovation and to building a safer digital ecosystem. This investment is fueling our next chapter of growth, allowing us to innovate faster, expand our product offerings, and deepen partnerships with brokers and policyholders. Heres to more innovation and growth in 2025!

Zurich shares our passion for innovation and our commitment to building a more secure digital ecosystem. Strengthening Partnerships Our broker partners and policyholders are at the heart of everything we do, and we are committed to continuing to deliver unparalleled value and support for them.

Rising temperatures, extended periods of drought, and the increasing frequency and severity of wildfires and other severe storms are reshaping insurance coverage and policyholder needs. But this can leave policyholders without coverage when they need it. Review and update policies regularly as climate risks continue to evolve.

According to Money.com , an independent publisher, recent year-over-year premium increases have averaged 20%, and policyholders should expect to see at least a 10-15% increase in 2024. Because of this, as the expenses of building a house increase, so will insurance premiums. Over the past few years, nearly every homeowner in the U.S.

Their comprehensive approach, combining expert knowledge, personalised service, and a keen attention to detail, has earned them a stellar reputation among policyholders and insurers alike. We look forward to continuing our mission of helping policyholders navigate the complexities of property damage claims with confidence and ease.”

Driven by rapid advancements in technology, shifting risks, and increasing policyholder expectations, the industry will likely have different products and services by the time 2025 draws to a close. The highly customizable nature of a UBI policy may appeal to cost-conscious policyholders or those who want more control over their premiums.

The rising costs of building or repairing properties have a direct effect on insurance premiums. With the increased cost of materials, labour, and other construction-related expenses, building or repairing properties has become more expensive. “Underinsurance is a major concern in the property insurance industry.

As policyholder expectations continue to evolve rapidly, insurance agents need to adapt quickly as well. Personalize communications and engagement with policyholders. Agents can send reminders of renewals, coverage updates, new product recommendations, and seasonal reminders targeting specific policyholder needs.

A special thank you goes to our exceptional employeesour Cowbellerswho dedicate themselves every day to not only providing outstanding service to our clients but also to building a safer and more resilient digital ecosystem for everyone. Looking to 2025, we are poised for exceptional growth and opportunity.

Simon has played a pivotal role in expanding our reach and building the robust foundation of our operational capabilities in the UK, aligned with a global vision. As we continue to build out our presence in the U.K. Simon Hughes has been appointed Senior Vice President of Global Distribution effective immediately.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content