This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When it comes to managing workers’ compensation, understanding classification rules is fundamental. These rules not only influence the amount you pay in premiums but also help ensure that your company is correctly classified based on the work it performs. This can free up resources for other areas of your business.

In this three-part series, we are examining nine elements of independent premium audits to help you better understand and control your workers’ compensationpremiums. These foundational aspects are crucial for ensuring accurate premium calculations and avoiding costly mistakes.

When an employer receives a revised workers’ compensationpremium bill, the accuracy of the bill can be uncertain and confusing. To ensure fairness and correctness, an independent premium audit is highly recommended. Payroll Information A critical step in any premium audit is the review of an employer’s payroll.

Many companies operate under an unwritten rule: accept every workers compensation claim, no questions asked. A well-managed workers compensation program should pay 100% of legitimate claimsand 0% of the claims that arent. Fight Fraud and Exaggerated Claims Workplace injury fraud is a significant cost driver in workers compensation.

In this final part of our series exploring the nine elements of independent premium audits, we turn our focus to specialized situations and nuanced adjustments auditors carefully evaluate. Auditors disallow estimates, making precise documentation vital to receiving the intended premium savings associated with this exception.

When it comes to calculating workers’ compensationpremiums, two critical factors play a significant role: the frequency and severity of claims. Understanding how these two factors interact can help businesses reduce their premiums and improve workplace safety.

When it comes to managing workers’ compensation, understanding classification rules is fundamental. These rules not only influence the amount you pay in premiums but also help ensure that your company is correctly classified based on the work it performs. This can free up resources for other areas of your business.

Workers’ compensation programs are a cornerstone of workplace safety and risk management. Exclusivity: Protection Against Lawsuits One of the most significant benefits of workers compensation for employers is the exclusive remedy provision. Litigation, especially in cases of workplace accidents, can be costly and time-consuming.

Navigating workers’ compensation can be complex, with various parties working together to ensure effective claims management and cost containment. Lets explore the roles of these critical players in a workers’ compensation system. Their expertise enhances the efficiency and accuracy of the claims process.

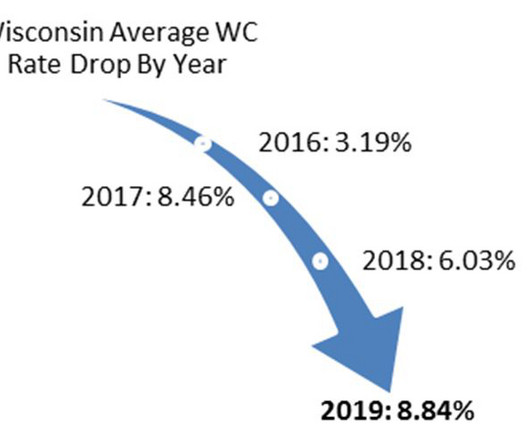

On October 1, 2024 Wisconsin continued its trend entering a ninth consecutive year of reduced workers compensationinsurance rates. Workers compensation rates are state mandated in Wisconsin, meaning all insurance carriers must use the same rates resulting in premiums from one carrier to another are basically the same.

By shifting your perspective from compliance-as-burden to compliance-as-advantage, you can leverage OSHA requirements to create a safer, more productive workplace, reduce workers compensation costs , and enhance your company’s reputation. You should consult with your insurancebroker, attorney, or qualified professional.

Individual Health Insurance Tax Deductibility If you offer individual health insurance to your clients, they may be able to include their health insurancepremiums in their medical expense calculation on their taxes. Plus, your clients can save on Federal Insurance Contribution Act (FICA) taxes and Workers Compensation.

A medical health insurancebroker helps you choose the best health insurance plan tailored to your needs. Unlike agents tied to one insurer, brokers work with multiple companies to give you unbiased options. What is a medical health insurancebroker?

Get a Quote Insurance under one roof We are specialists in many types of insurance GET YOUR QUOTE GET YOUR QUOTE 1. The Financial Toll of a Liability Claim A lawsuit can lead to crippling legal expenses, compensation payouts, and increased insurancepremiums.

Effectively managing workers compensation requires careful oversight and proactive measures to identify and prevent fraudulent or exaggerated claims. Large claims can have significant long-term impacts on premiums, experience modification factors, and overall workers’ compensation costs. All state laws vary.

Click Link to Access Free PDF Download “How to Calculate Your Minimum Experience Mod, Controllable Premium & the Revenue Impact” Things that we don’t understand can seem a lot more difficult than they actually are. This is the actual costs of the claims that were legitimate claims for workers’ compensation.

Block of Flats Insurance with Unoccupied Cover A tailored policy that protects both occupied and vacant flats within the same building. Loss of Rent Cover If a flat becomes uninhabitable due to an insured event, this can help compensate for lost rental income. Looking for a quote now?

” If you don’t have the opportunity to check out the full webinar, read on for key insights from the discussion and actionable advice for insurers, brokers, and policyholders. And when you take into consideration that Direct Premiums Written (DPW) increased by 2.0%

So this is your premium adjustments, and these are discretionary adjustments that can be given by your underwriter based on how well they perceive you managing your risk, how well they perceive you managing your risk. You’re gonna have to some of these premium adjustments. We’ve got things under control based on your mod.

However, for insurancebrokers, the wide spectrum of restaurants represents both a challenge and an opportunity. With thousands of restaurants in Charlotte and across North Carolina, the need for comprehensive insurance coverage is vital.

In this article, we’ll explain the benefits of using a broker, how to find a reliable one, and key questions you should ask. Key Takeaways Medical insurancebrokers serve as intermediaries, helping clients navigate the insurance market and find suitable health plans tailored to their unique needs.

Get a Quote Insurance under one roof We are specialists in many types of insurance GET YOUR QUOTE GET YOUR QUOTE Key Takeaways Consistent rate increases have been experienced in the property insurance market since 2017. Inflation drives up property valuations , construction costs , and insurancepremiums.

The global insurancebroker and risk advisor’s survey of more than 1,300 captives also shows that gross written premiums in this area grew from $54 billion in 2019 to nearly $61 billion in 2020. For many organizations, captive insurance provides a viable alternative for these risks.

Commercial Flood Insurance in the United Kingdom: Types of Coverage Available Commercial flood insurance policies typically cover: Property Damage: Repair or replacement of buildings, fixtures, and equipment. Business Interruption: Compensation for lost income during downtime caused by flooding.

Policies with shorter maximum benefit periods typically have lower premiums. State STD vs. Voluntary The California State Disability Insurance (SDI) program provides short-term and Paid Family Leave (PFL) to eligible workers when off work due to a non-work-related illness or injury, pregnancy, or childbirth.

The alleged plan: to deliberately misrepresent the ACA’s advance premium tax credits – APTC – which are paid directly to an insurance company, not to the consumer. First, the American Rescue Plan (ARP) enhanced Marketplace premium subsidies starting in mid-2021.

You earn the same commission (and bonuses) as you would on your own, working as an independent broker. Word & Brown does not earn its compensation from your commissions. and Voluntary coverage from leading insurers and administrators for Small Group and Large Group. The selected carrier or administrator pays us directly.

Sell the value Make sure you talk with your customer about what makes the product you’re recommending a better choice for their specific situation, as compared to something from another carrier (or another broker). If carrier A has a plan that includes a similar network, but the premiums are lower, it’s okay to sell based on cost.

Slip and Trip Claims Property owners’ liability insurance provides protection against the costs associated with third-party claims, such as slips and trips. Slips and trips are quite a common claim these days, helped to an extent by the compensation culture that has emerged and the rise of no-win, no-fee legal services.

In practice, there may be many variations and additional elements of cover provided by your landlord insurance policy (such as the loss of rental income that we have already mentioned) – and it is typically a broker’s responsibility to help you understand what those additional areas are and how they might benefit you.

In the event of a loss, having a comprehensive home inventory can help policyholders prove the existence and value of their belongings to ensure proper compensation. Moreover, policyholders should refrain from initiating extensive repairs until insurance adjusters have assessed the damage.

Most Marketplace enrollees qualify for premium tax credits (premium subsidies). 17 Premium subsidies are a tax credit based on the total annual income earned by everyone in the enrollee’s tax household (everyone listed on your tax return). Most Marketplace enrollees qualify for premium tax credits (premium subsidies).

Click Link to Access Free PDF Download “How to Calculate Your Minimum Experience Mod, Controllable Premium & the Revenue Impact” Whatwe’retryingtodohere,whatdidnotwhatnecessarilywe,whattheinsurancecarriers,whattheunderwriterstryingtodoisthey’retryingtogetanaccurateperceptionofrisk. All state laws vary.

Commercial property insurance is a key component in this protection, offering a safety net against unexpected disasters. Whether you own a quaint little shop or a sprawling office complex, securing proper insurance means youre prepared for the unexpected. Another myth is that your landlord’s insurance covers your business assets.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content